Owner Compensation

Owner Draws vs Salary: The Bookkeeping Side

May 25, 2026

You took $4,000 out of the business last Tuesday to cover rent. Your bookkeeper categorized it as "Owner draw." Your accountant moved it to "Wages" at year-end. The grocery run from the same week — paid on the business credit card — landed in "Office supplies." Half of the bookkeeping cleanup work on the average small-business file is categorizing what the owner spent and how they took it out.

This post covers the bookkeeping side of owner draws, salary, and dividends — what gets categorized as what, what NOT to run through the business, and the year-end cleanup pattern most accountants quietly do every year. The tax-strategy side (which is right for your situation) belongs to your accountant; the Modern Axis "Salary vs Dividends" post is the deep version of that decision.

Key takeaways

Sole proprietors don't get salary — they take draws. Draws are not a business expense; they're a reduction of owner equity on the balance sheet. The tax happens on the business's net income, regardless of how much the owner drew.

Incorporated owners can choose salary, dividends, or both. Salary is an expense on the P&L and triggers source deductions (CPP, EI, income tax withholding). Dividends are not a P&L expense — they're a distribution of after-tax profit, recorded as a reduction of retained earnings on the balance sheet.

Personal expenses run through the business are the largest cleanup category on most small-business files. The right rule: if it's not 100% business, don't put it on the business card.

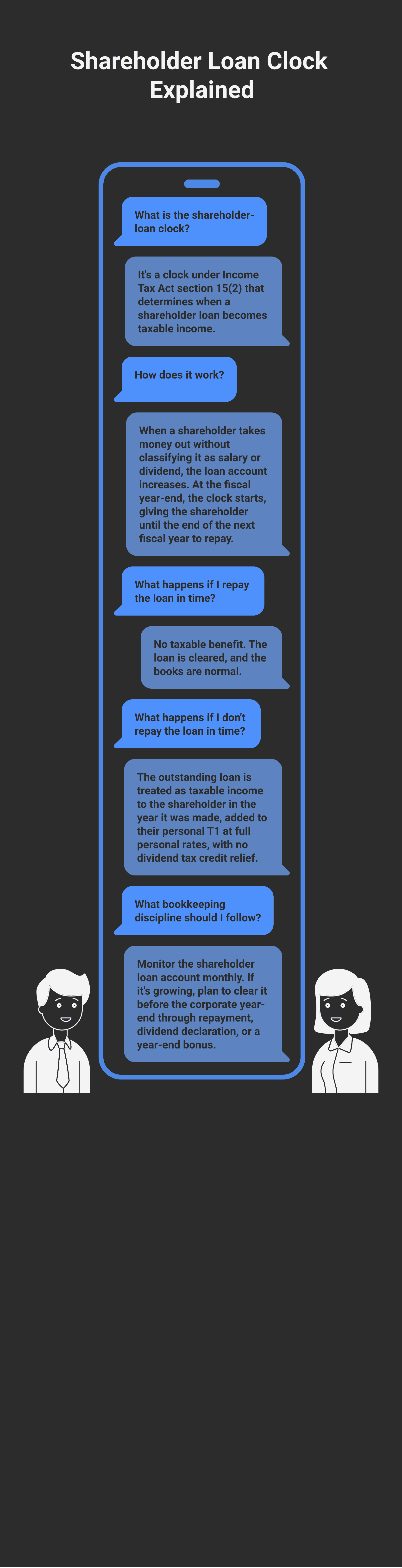

Shareholder loan accounts are not slush funds — section 15(2) of the Income Tax Act treats certain outstanding shareholder loans as taxable income to the shareholder if not repaid within one year of the corporate year-end. The bookkeeping discipline of clearing the shareholder loan account every year matters for both the books and the tax bill.

Year-end is when the accountant reclassifies six months of "Office supplies" and "Travel" entries. Cleaner monthly categorization on the bookkeeping side saves several hours of professional time at year-end.

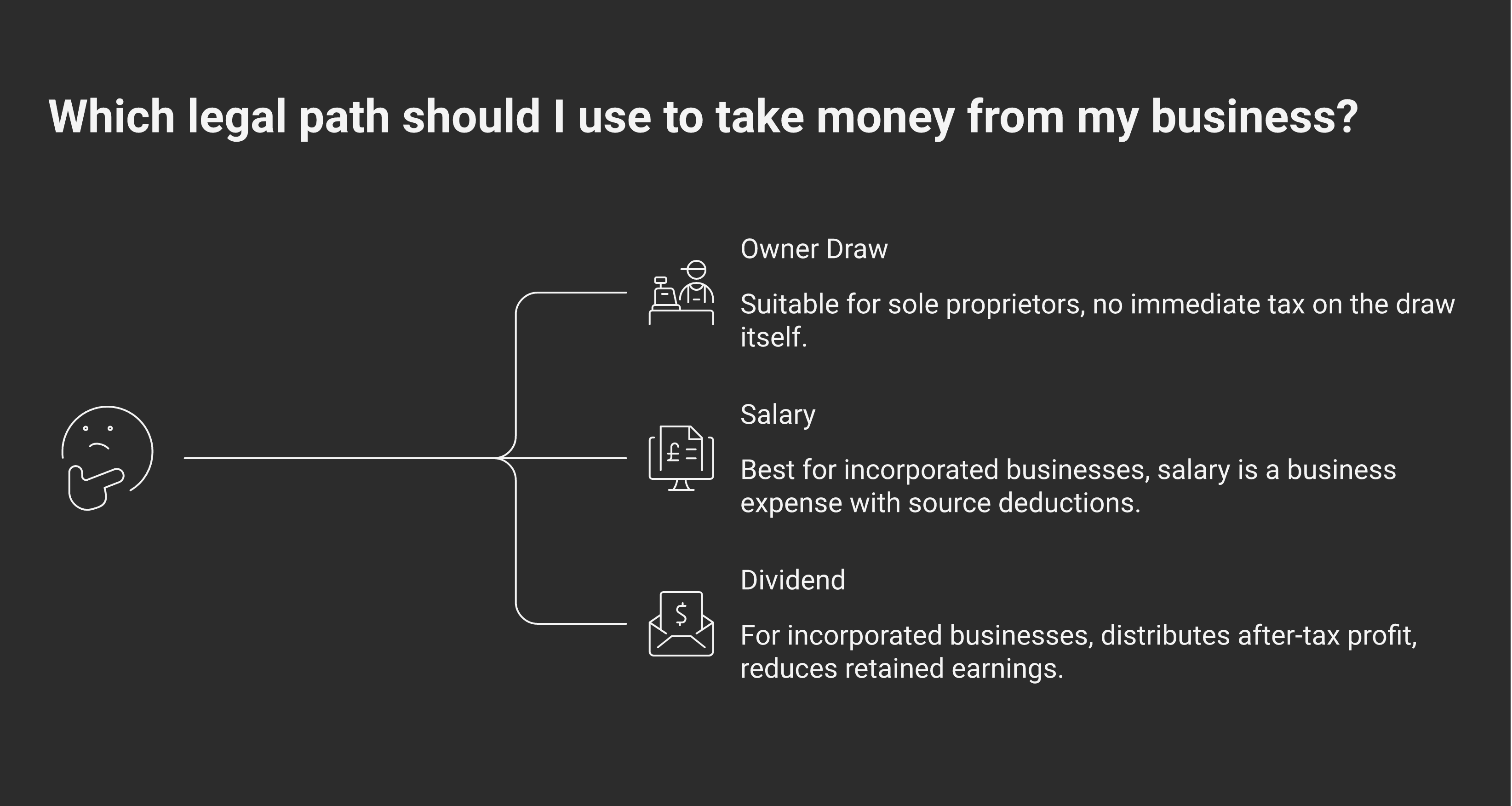

The three ways an owner takes money out

Before the bookkeeping side, the three legal paths money leaves a business and lands in the owner's pocket:

Draw (sole proprietors only). The owner takes cash. No tax happens on the draw itself; tax is on the business's net income, calculated at year-end on the T1's T2125 form. Draws reduce owner equity on the balance sheet.

Salary (incorporated businesses). The corporation pays the owner like any other employee. The salary is a deductible expense on the corporation's P&L. Source deductions apply: CPP, EI (unless owner-manager exempt), and income tax are withheld and remitted by the 15th of the following month.

Dividend (incorporated businesses). The corporation distributes after-tax profit to shareholders. The dividend is not a P&L expense — the corporation's net income is calculated before dividends. Dividends reduce retained earnings on the balance sheet. The shareholder reports the dividend on their personal T1 with the gross-up and dividend tax credit mechanism.

Most incorporated owners use a mix of salary and dividends. The decision of which mix is right for your specific situation depends on multiple variables — RRSP room, CPP contributions, family income split, expected future sale of the business — and is the kind of conversation that belongs in an accountant's office, not in a bookkeeping software setting. The Modern Axis "Salary vs Dividends" post walks through that decision in detail; this post focuses on what your books need to look like once the decision is made.

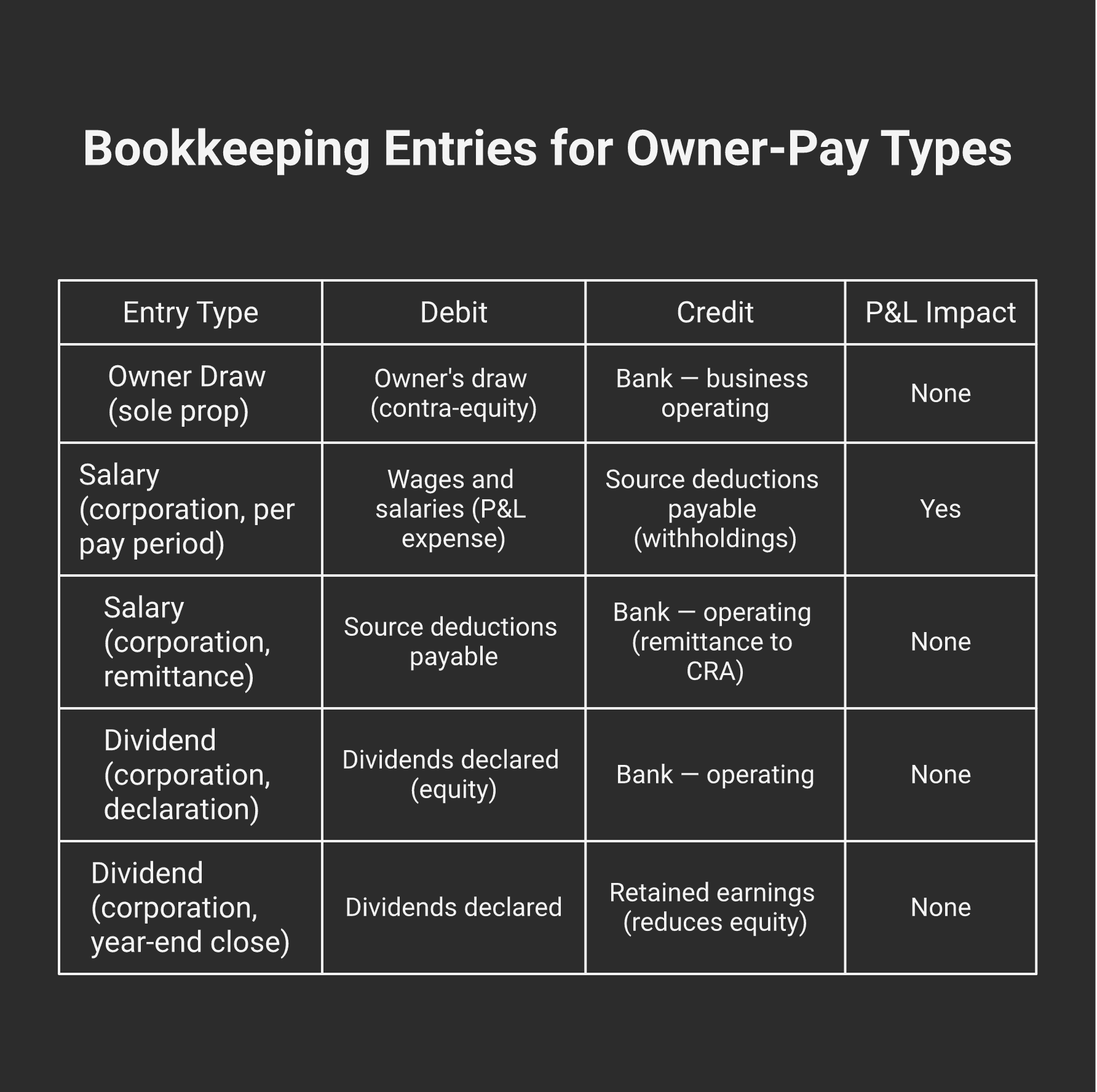

How each gets recorded

Sole proprietor draws

On a sole prop's books, the draw flow is:

Cash transfer from business account to personal account

Bookkeeper records: debit "Owner's draw" (a contra-equity account, reduces owner equity), credit "Bank — business operating"

No expense hits the P&L

At year-end, the "Owner's draw" account balance is closed into "Owner's capital" — the running equity account on the balance sheet

A common bookkeeping error: categorizing draws as a business expense. Travel that the owner took for personal reasons, recorded as "Travel - business," shows up on the P&L as a deduction the business doesn't actually have. The CRA's audit position is consistent — personal expenses are not deductible, regardless of which account they were posted to.

Salary on incorporated books

The corporation runs the owner on payroll like any other employee:

Each pay period: debit "Wages and salaries" (expense), debit "Wages payable" or directly credit "Bank — operating" (the net pay), and credit "Source deductions payable" (the withholding)

The 15th of the next month: debit "Source deductions payable", credit "Bank — operating" (the remittance to CRA)

Year-end: the corporation issues the owner a T4 alongside other employees' T4s

The bookkeeping discipline is identical to any other employee — the only thing different is that the employee is also the shareholder. See the source-deductions-for-first-time-employers post for the full payroll flow.

Dividends on incorporated books

Dividends are declared by the corporation's directors (in a small CCPC, the owner-manager is usually the sole director, so this is a formality on paper but a real step nonetheless):

The declaration: a board resolution (or sole-director resolution) authorizing the dividend

Payment: debit "Dividends declared" (an equity account), credit "Bank — operating"

Year-end: "Dividends declared" closes into "Retained earnings" — reducing the running retained earnings balance on the balance sheet

T5 slip: the corporation issues the shareholder a T5 reporting the dividend by the end of February following the calendar year of the dividend

Dividends never appear on the P&L. They're not a deduction. The corporation pays tax on the net income that produced the dividend; the shareholder pays tax (with credit) on receiving it. This is integration.

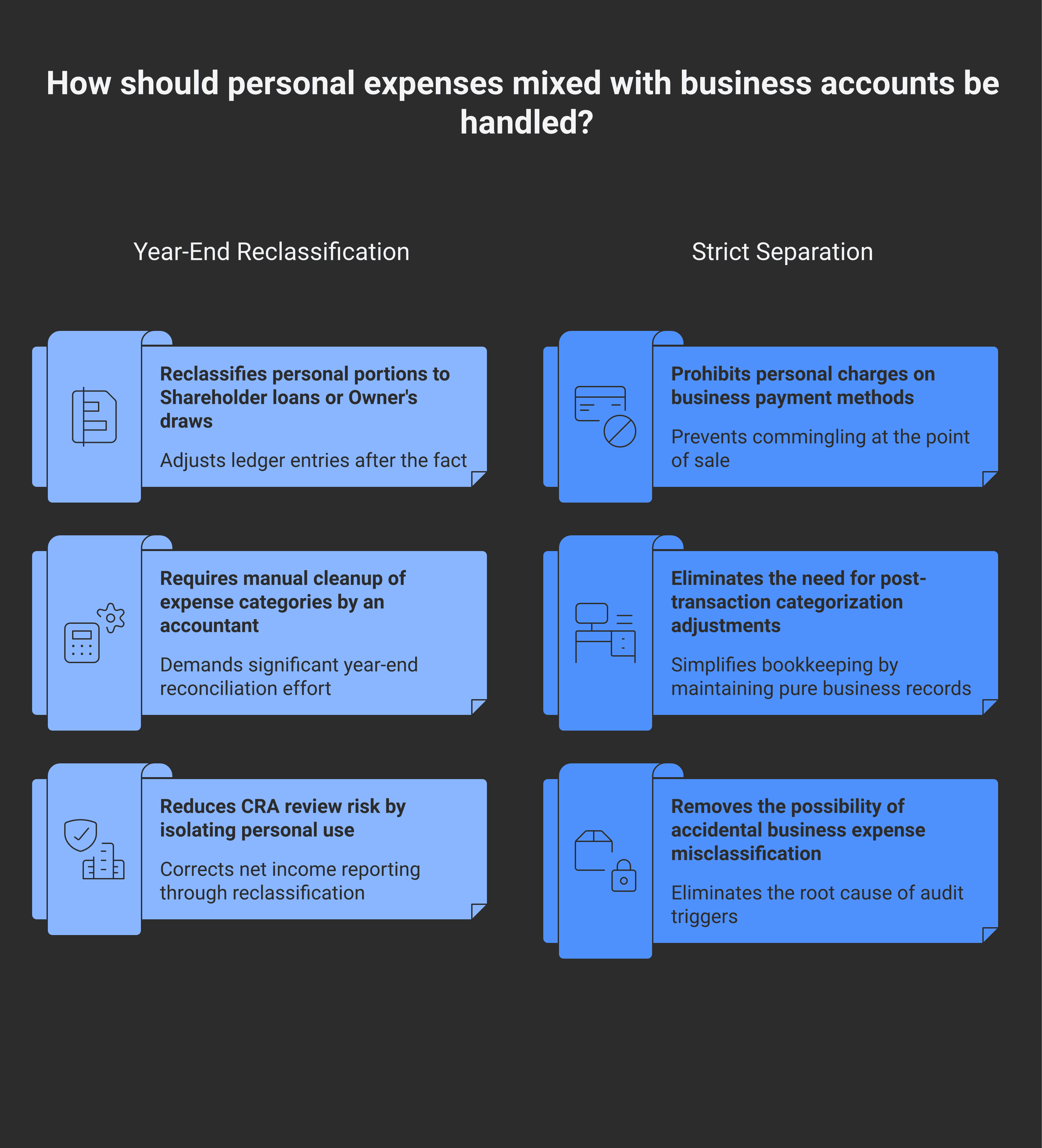

The personal-expenses-run-through-the-business problem

Half of the cleanup work on a typical small-business file is sorting personal expenses that got run through the business card or business account. The classic categories:

Groceries posted as "Office supplies" or "Meals and entertainment"

Personal car expenses (gas, repairs, insurance) posted as "Vehicle expense" with no mileage log

Home cellphone and internet posted at 100% when the actual business-use percentage is 60–70%

Personal travel posted as "Travel" without a business-purpose record

Family meals posted as "Meals and entertainment" without a client present

Gym memberships, personal subscriptions posted as business expenses

The CRA's position is consistent: only the business-use portion is deductible. Personal expenses run through the business get reclassified to a shareholder loan account (for corporations) or a draw (for sole props) at year-end. The accountant identifies them, reclassifies them, and the books end the year showing the correct net income.

The cleaner approach: don't run personal expenses through the business in the first place. The right rule is simple — if it's not 100% business, don't put it on the business card. Mixed-use items like cellphones and home internet are an exception (use a documented allocation), but groceries, personal travel, and family meals never belong on the business books.

The cost of the alternative: at minimum, several hours of accountant time at year-end to clean up. At maximum, a CRA review that disallows expenses and assesses tax plus penalty.

Shareholder loans — the most-misunderstood account

For incorporated owners, the shareholder loan account is where money the owner has put into or taken out of the corporation (outside of formal salary or dividend) lands. It works both ways:

Shareholder loan payable (liability): the corporation owes the owner. Happens when the owner puts money in — funded a startup, lent the corporation cash to bridge a payroll gap, paid corporate expenses from a personal card.

Shareholder loan receivable / due from shareholder (asset): the owner owes the corporation. Happens when the owner takes money out without classifying it as salary or dividend, or when personal expenses get reclassified.

The trap: a shareholder loan receivable (owner owes the company) that remains outstanding at the corporation's year-end and isn't repaid within one year is treated under section 15(2) of the Income Tax Act as taxable income to the shareholder. The amount gets added to the shareholder's personal T1 — at full personal rates, with no dividend tax credit relief. This is one of the more expensive surprises in owner-manager bookkeeping.

The bookkeeping discipline: monitor the shareholder loan account monthly. If the owner-owes-corporation balance is growing, plan to clear it before the corporate year-end — either by repayment, by declaring a dividend that offsets the loan, or by recording a year-end bonus (salary). The Modern Axis "Should You Incorporate" post covers the structure choice that creates this dynamic in the first place; the Modern Axis "Small Business Deduction" post covers the related corporate-level tax that informs the year-end choice.

What the accountant does at year-end

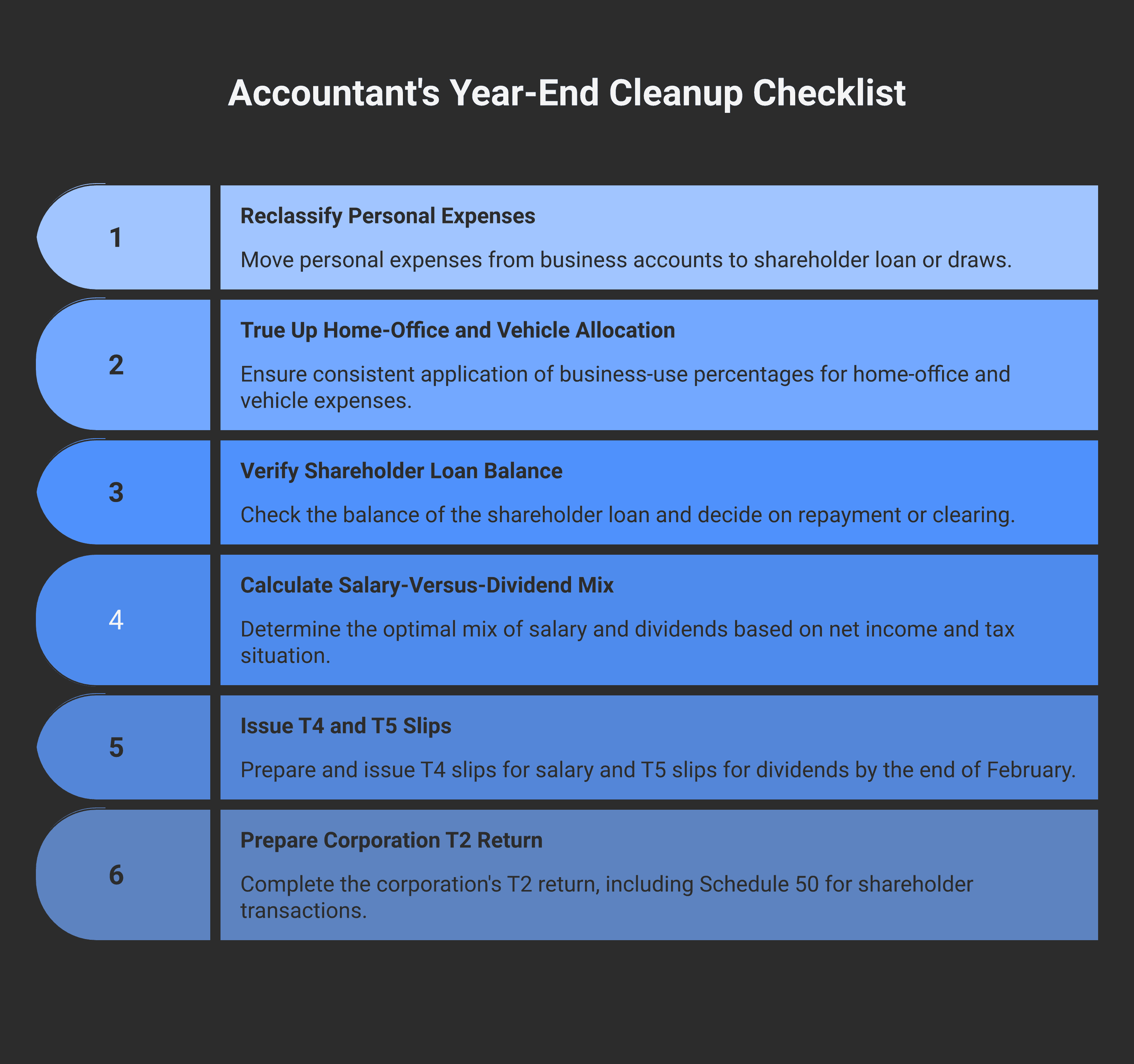

The cleanup pattern most accountants apply to owner-manager books at year-end:

Reclassify personal expenses out of business expense accounts and into shareholder loan (or draws for sole props)

True up the home-office and vehicle allocation — the business-use percentage of cellphone, internet, and vehicle expenses, applied consistently across the year

Verify the shareholder loan balance and decide whether to clear it through dividend, bonus, or repayment before the next year-end

Calculate the salary-vs-dividend mix for the year if it wasn't pre-set — the decision often happens at year-end based on actual net income and the owner's personal tax situation

Issue T4s (for salary) and T5s (for dividends) — both by the end of February following the calendar year for which they apply

Prepare the corporation's T2 return — Schedule 50 reports shareholder transactions for owner-manager corporations

Cleaner monthly bookkeeping shortens this list. The biggest single saving: not running personal expenses through the business card in the first place, so step 1 takes thirty minutes instead of three hours. The second-biggest saving: clearing the shareholder loan account monthly, not annually.

When monthly owner-comp categorization gets done by a bookkeeper

Modern Books categorizes owner pay each month with the salary-vs-dividend mix that the accountant set at year-end, runs payroll on the salary portion, processes dividend declarations against retained earnings, and monitors the shareholder loan account so it doesn't drift toward the section 15(2) one-year clock. The Personal Income Tax in Canada post on Modern Axis covers the personal-side tax mechanics; this is the bookkeeping that makes it work. Modern Books' Mid and Growth tiers include this as part of monthly bookkeeping for incorporated owner-managers. More in the Modern Books resource hub.

Frequently asked questions

What's the difference between owner draws and salary in Canada?

Owner draws apply to sole proprietors — the owner takes cash out of the business, with no tax happening on the draw itself; tax is calculated on the business's net income on the T1's T2125. Salary applies to incorporated businesses — the corporation pays the owner like any other employee, including source deductions (CPP, EI, income tax). Sole props can't take salary; incorporated owners can choose salary, dividends, or both.

How are owner draws recorded in bookkeeping?

A draw is recorded as a debit to "Owner's draw" (a contra-equity account that reduces owner equity) and a credit to the business bank account. It does not appear on the P&L as an expense. At year-end, the draw balance is closed into the running "Owner's capital" equity account on the balance sheet. Common error: categorizing draws as a business expense — this overstates expenses and understates net income.

Do I need to take source deductions on my own salary?

Yes, if you're an incorporated owner paying yourself salary. The corporation has to withhold CPP and income tax from your salary and remit by the 15th of the following month. EI is usually exempt for owner-managers who own more than 40% of voting shares, but verify your situation. See the source-deductions-for-first-time-employers post for the full mechanics.

What happens if I run personal expenses through the business?

The accountant reclassifies them at year-end — moving the personal portion out of business expense accounts and into shareholder loan (corporation) or draws (sole prop). The CRA can disallow expenses on review if they're clearly personal. The cleanup work compounds the longer it goes uncorrected, and at scale becomes a multi-thousand-dollar audit-cleanup project. The right discipline: if it's not 100% business, don't put it on the business card.

What's a shareholder loan and why does it matter?

A shareholder loan account tracks money that's moved between the corporation and the shareholder outside of formal salary or dividends. It can be a liability (corporation owes the shareholder) or an asset (shareholder owes the corporation). The trap: an asset-side shareholder loan that remains outstanding at year-end without repayment within one year is treated under Income Tax Act section 15(2) as taxable income to the shareholder at full personal rates. Monitor the balance monthly.

Is dividend payment a deductible expense for the corporation?

No. Dividends are not deductible. The corporation pays corporate tax on its net income first; dividends are paid from after-tax retained earnings. This is part of Canada's tax integration system — the corporation pays tax, the shareholder pays tax on receipt with a credit, and the combined burden is meant to approximate what the owner would have paid as an individual. Salary, by contrast, is fully deductible to the corporation.

How does the salary-vs-dividend decision affect my bookkeeping?

Salary creates a payroll workflow (monthly source-deduction remittances, T4 at year-end). Dividends create a balance-sheet workflow (a board resolution, a credit to "Dividends declared", a T5 at year-end). Most owner-managers use a mix, set by the accountant at year-end. The bookkeeper executes the mix throughout the year; the strategic decision is the Modern Axis "Salary vs Dividends" post's territory.

What's the biggest year-end cleanup item for owner-manager bookkeeping?

Reclassifying personal expenses out of business expense accounts is consistently the largest single cleanup item. A typical owner-managed file has a handful of grocery runs, personal travel charges, family meals, and home-cellphone overruns posted as business expenses through the year. The accountant moves them to shareholder loan (or draws) at year-end. The cleaner alternative: don't run personal expenses through the business in the first place.

General information only — not tax or compliance advice. The right salary-vs-dividend mix, the right shareholder-loan management strategy, and the right approach for your specific business depend on facts not covered here. Talk to a CPA who knows your numbers and your personal tax situation before relying on anything you've read.