Payroll

Source Deductions for First-Time Employers in Canada

May 25, 2026

You hired your first employee. You agreed on a salary. You're about to cut the first cheque. The piece nobody explained: the CRA expects you to remit Canada Pension Plan, Employment Insurance, and income tax withholdings every month from that point forward — and the penalty meter starts on the first missed deadline, not on the third or the tenth.

This post covers what source deductions are, what every first-time Canadian employer is required to withhold and remit, how the CRA decides which remitter class you fall into, and the day-one penalty structure that catches new employers off guard.

Key takeaways

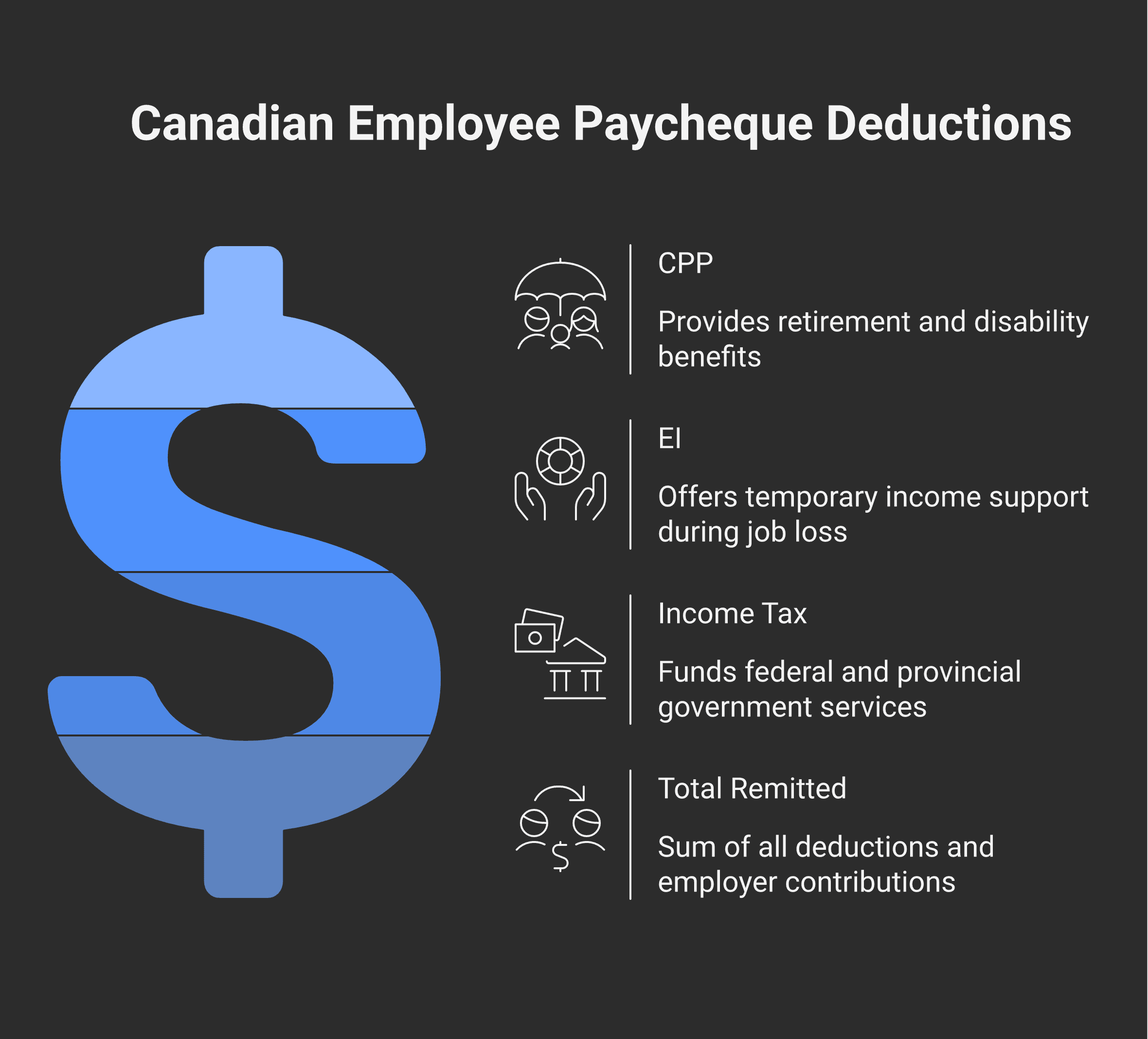

Three things get withheld from every employee's pay: Canada Pension Plan (CPP), Employment Insurance (EI), and income tax. The employer also pays a matching share of CPP and an EI share (1.4× the employee EI deduction).

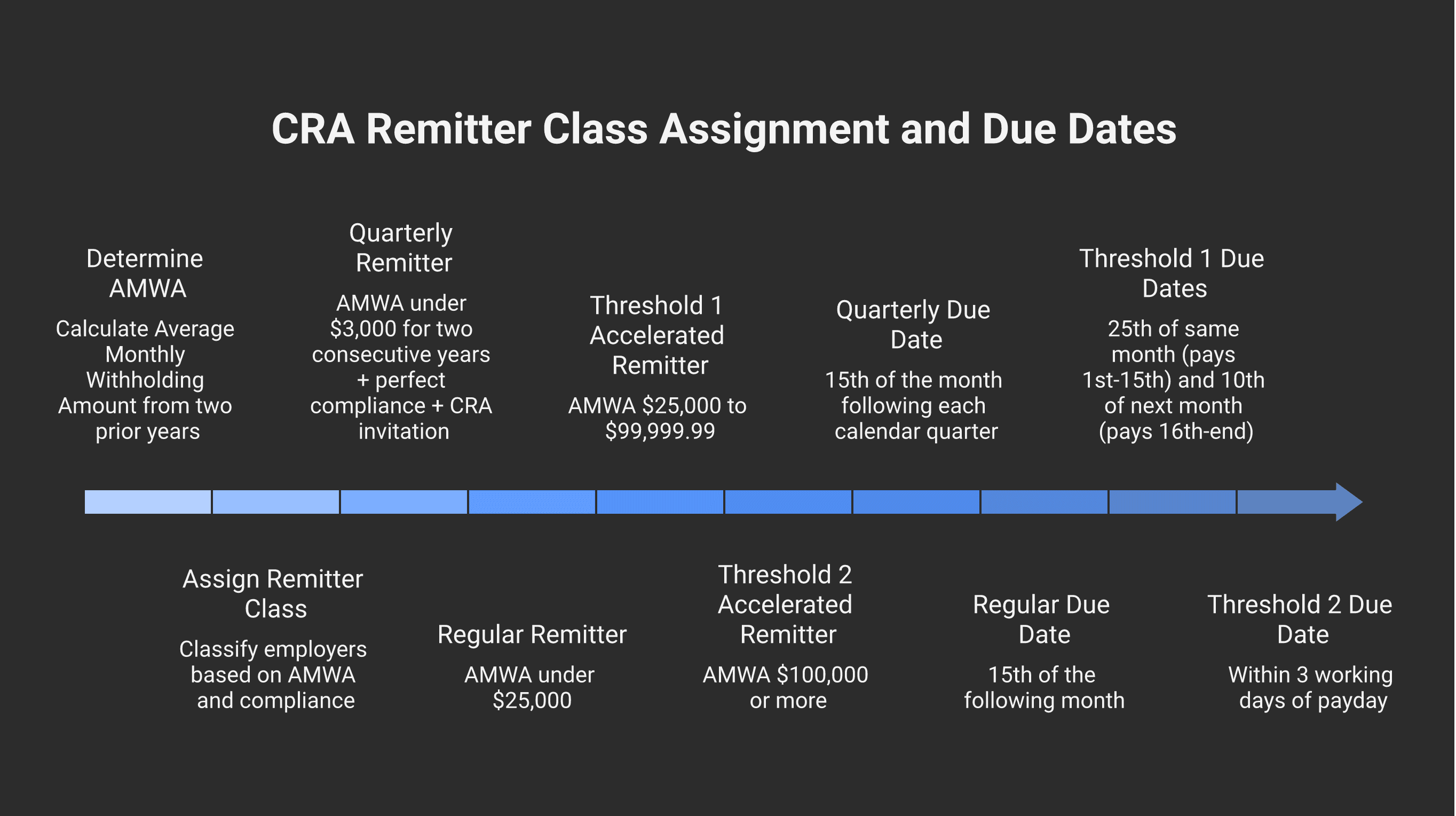

The CRA assigns every employer a remitter class based on Average Monthly Withholding Amount (AMWA) from two years prior. First-time employers are regular monthly remitters by default — payments due the 15th of the following month.

The PD7A is the statement of account the CRA uses to communicate remitter class, due dates, and balance owing. Mailed to regular and quarterly remitters; electronic remitters don't receive it.

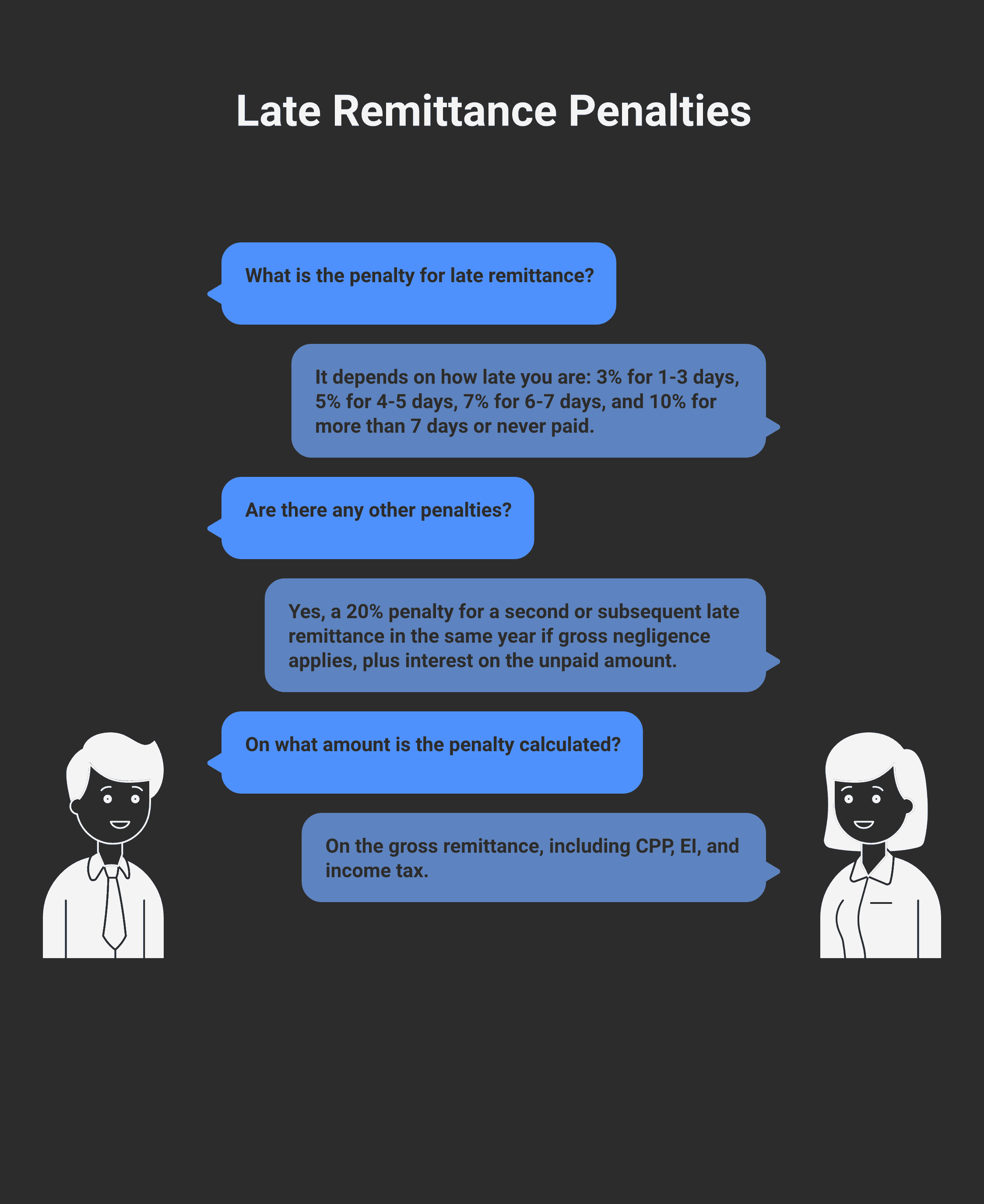

Penalties for late remittance start at 3% and scale to 10% depending on how late, with a 20% rate on second offences within the same year if gross negligence applies. These apply per remittance, not per payroll cycle.

Paying yourself as the owner-manager is also payroll if you structure compensation as salary. Set up the payroll account before the first cheque clears — back-filing is more expensive than getting it right from the start.

The rule, in one sentence

Under section 153 of the Income Tax Act, every Canadian employer who pays salary, wages, or other employment income is required to withhold income tax, CPP contributions, and EI premiums at source and remit them to the Receiver General by the due date for the employer's assigned remitter class.

That obligation kicks in the moment you cut a paycheque — not when you "feel like" a real employer, not when revenue hits a threshold, not after a grace period. Day one.

What you're actually withholding

Every employee paycheque has three deductions taken at source:

Canada Pension Plan (CPP) — both the employee and the employer contribute. The employee contribution is deducted from gross pay; the employer matches it dollar-for-dollar and remits both halves. CPP2 (the second-tier contribution on earnings between the YMPE and YAMPE) is now fully phased in and applies in addition to base CPP.

Employment Insurance (EI) — the employee pays the base rate as a percentage of insurable earnings up to the annual maximum. The employer pays 1.4× the employee EI deduction. Some workers (most owner-managers who own more than 40% of voting shares) are EI-exempt; treat that as the exception and verify before applying it.

Income tax — federal and provincial combined. Calculated using the CRA's payroll deductions tables (or the CRA's Payroll Deductions Online Calculator) based on the employee's TD1 federal and provincial forms.

The total you remit each month is the sum of all three deductions across all employees, plus the employer's CPP match and 1.4× EI share.

Where the money goes and when

The CRA tracks every employer's source-deduction account through a document called the PD7A (Statement of Account for Current Source Deductions). The PD7A confirms your remitter class, lists each period's due date, and shows your balance owing.

You'll see a PD7A in the mail if you're a regular or quarterly remitter — but only until the CRA's paperless transition is complete. After that, all PD7A statements arrive in My Business Account electronically. Employers who remit through online banking (the most common method) typically don't see paper PD7As at all; the statement is generated on demand inside My Business Account.

Remittance is made through one of three channels:

Online banking through your business bank account (most common — uses the 15-character payroll account number, format

123456789RP0001)CRA My Payment (direct debit through the CRA portal)

Cheque to the Receiver General with the PD7A remittance voucher attached (slowest; not recommended)

The clock starts when the cheque clears your account or the electronic remittance is posted, not when you initiate it.

The remitter class you're in — and how it changes

The CRA assigns every employer one of four remitter classes based on Average Monthly Withholding Amount (AMWA) from two calendar years prior:

Class | AMWA (two years prior) | Due date |

|---|---|---|

Quarterly | Under $3,000 for 2 consecutive years + perfect compliance + CRA invitation | 15th of the month following each calendar quarter |

Regular (monthly) | Under $25,000 | 15th of the following month |

Threshold 1 (accelerated) | $25,000 – $99,999.99 | 25th of same month (for pays 1st–15th) and 10th of next month (for pays 16th–end) |

Threshold 2 (accelerated) | $100,000 or more | Within 3 working days of payday |

A first-time employer is always a regular (monthly) remitter to start. The class can only change after you've had two full calendar years of payroll history and the AMWA crosses one of the thresholds. CRA notifies you in writing if your class changes — your remitter status doesn't change because you started paying more in a single month.

The quarterly class is invitation-only. You don't apply for it; the CRA invites employers who qualify. If you're new and you want to know whether you're a candidate, the answer is: not for at least two years.

The penalty structure that starts day one

The CRA's late-remittance penalties under section 227 of the Income Tax Act are graduated by lateness, not by amount. They apply per remittance:

3% if the remittance is 1 to 3 days late

5% if 4 to 5 days late

7% if 6 to 7 days late

10% if more than 7 days late, or if amounts are deducted but never remitted

A second or subsequent late remittance in the same calendar year can attract a 20% penalty under the gross negligence rule. Interest also runs on the unpaid amount at the CRA's prescribed rate.

The penalties are calculated on the gross remittance amount — the full CPP + EI + income tax total — not the income tax portion alone. That's why even a one-day-late payment on a $4,000 remittance is a noticeable hit, and why the cleanest practice is to schedule the bank transfer for the 12th or 13th of the month rather than the 15th itself.

The owner-manager exception (and the trap)

If you're a sole proprietor paying yourself out of business cash, there are no source deductions — you draw, the business income passes through to your T1, and you pay tax through instalments. (See our cash-vs-accrual post for the related bookkeeping side.)

If you've incorporated and you're paying yourself salary from the corporation, source deductions apply to you exactly the same way they apply to any other employee. The corporation withholds CPP, EI (unless you qualify for the owner-manager EI exemption), and income tax from your salary, remits monthly, and issues you a T4 at year-end. The choice of how to pay yourself — salary, dividends, or a mix — has different tax consequences; the Modern Axis "Salary vs Dividends" post walks through that decision. From a bookkeeping perspective, the moment you choose salary, source deductions become non-optional.

The trap: an incorporated owner who pays themselves an irregular salary throughout the year, doesn't set up a payroll account, and tries to "true up" the withholdings at year-end. The CRA's view is consistent — if you pay yourself salary, you owe source deductions on that salary by the next 15th, regardless of whether the bookkeeping has been kept current.

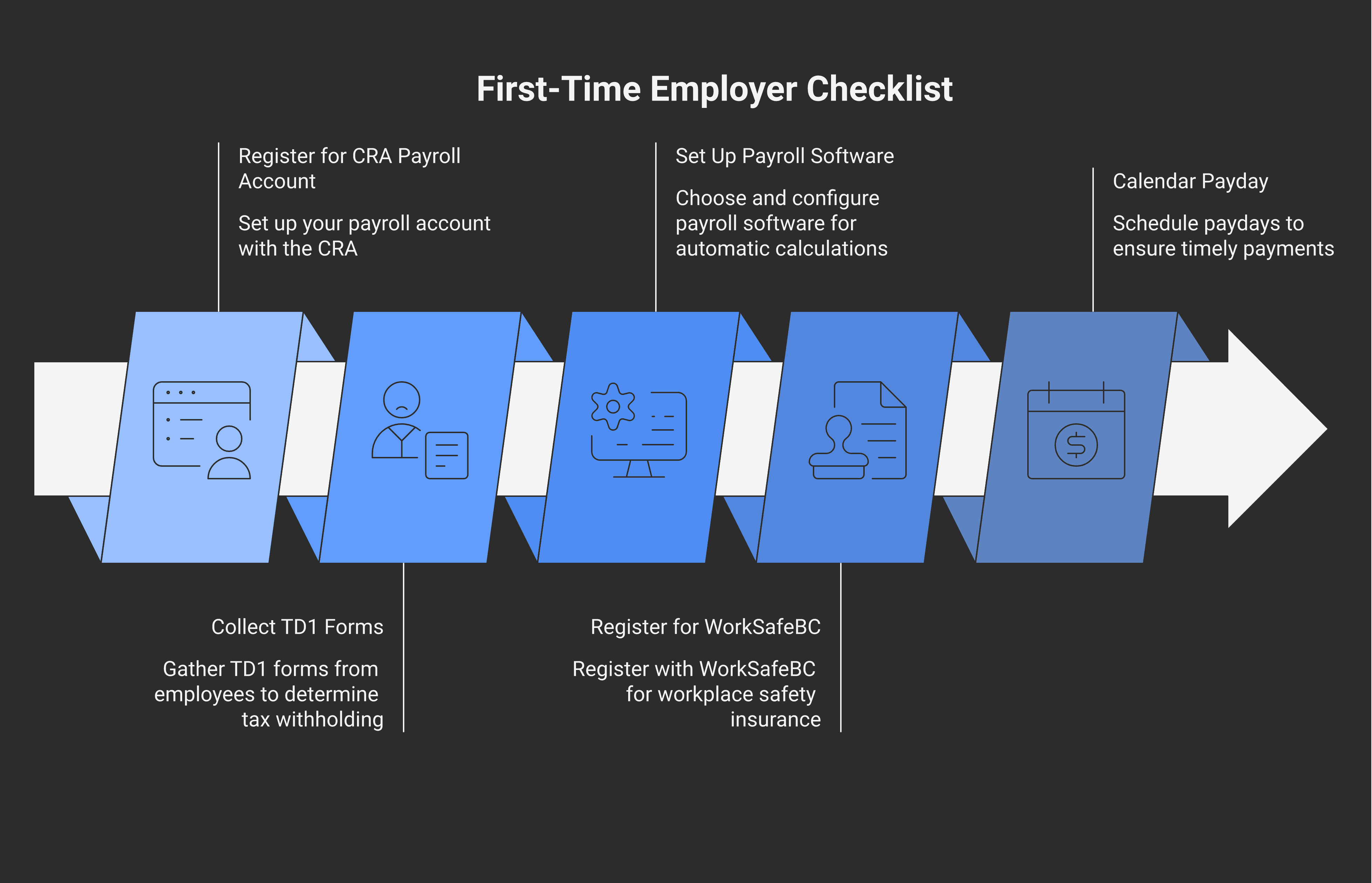

What to set up before you cut the first cheque

The mechanical checklist for any first-time Canadian employer:

Register for a CRA payroll account through My Business Account. This adds an RP suffix to your existing business number (the 15-character payroll account number described above). The CRA's My Business Account is also where you'll authorize your bookkeeper or accountant as a representative.

Collect a TD1 federal and a TD1 provincial form from every employee at hire. These tell your payroll software how much income tax to withhold.

Set up payroll software that calculates CPP, EI, and income tax automatically. Most small businesses use QuickBooks Online Payroll, Wagepoint, or Payworks. Avoid manual calculation past the second or third employee — the rates and brackets change annually and the audit cost of a wrong remittance compounds.

Set up WorkSafeBC (or your provincial equivalent) if you're in British Columbia. WCB is separate from source deductions and has its own registration, classification, and quarterly reporting. Most provinces require registration before the first day of work.

Calendar the 15th of every month, in advance, for the next twelve months — and remit a few days early to avoid the bank-transfer-clears-late edge case. The penalty meter doesn't care that you initiated the transfer on the 14th if the funds posted on the 16th.

When the payroll side lands on a bookkeeper

Modern Books handles monthly payroll for Mid and Growth-tier clients — running the CPP, EI, and income tax calculations, issuing pay stubs, filing remittances on time, and producing T4s at year-end. If you're at the "first employee" milestone and don't want to learn the CRA's penalty schedule by experience, the Mid tier ($300/month) includes payroll for up to three employees. Catch-up work on a payroll account that's slipped behind is its own service — book a session if you've missed a few remittances and want to know what cleanup looks like.

Frequently asked questions

What are source deductions in Canada?

Source deductions are the CPP, EI, and income tax amounts a Canadian employer is required to withhold from each employee's gross pay and remit to the Canada Revenue Agency. The obligation applies under section 153 of the Income Tax Act and starts the day you issue your first paycheque, not after revenue or employee-count thresholds. Owner-managers paying themselves salary from a corporation are subject to the same rules as any other employee.

What's the deadline for remitting source deductions?

For a first-time employer (a regular monthly remitter), the deadline is the 15th of the month following the pay period. Pay an employee in March; remit by April 15. Late remittance triggers a graduated penalty — 3% if 1–3 days late, scaling to 10% if more than 7 days late, with a 20% penalty for repeat failures in the same year under gross negligence rules.

What's a PD7A?

The PD7A (Statement of Account for Current Source Deductions) is the document the CRA uses to confirm your remitter class, list each period's due date, and show your balance owing. Regular and quarterly remitters historically received it in the mail; following the CRA's paperless transition, statements arrive in My Business Account electronically. Employers who remit through online banking typically don't see paper PD7As at all.

Do I need to remit if I only pay myself as an incorporated owner?

Yes, if you pay yourself salary. The corporation has to withhold CPP and income tax from your salary cheque and remit by the next 15th. (EI is typically exempt for owner-managers who own more than 40% of voting shares, but verify your situation.) Source deductions are not optional based on how you "feel" about your role — they're triggered by salary payments, full stop. If you pay yourself dividends instead, source deductions don't apply (but the corporation has different reporting requirements — see Modern Axis on salary vs dividends).

How is my remitter class assigned?

The CRA assigns every employer one of four classes — Quarterly, Regular (monthly), Threshold 1 accelerated, Threshold 2 accelerated — based on the Average Monthly Withholding Amount (AMWA) from two calendar years prior. First-time employers are regular monthly remitters by default. Your class changes only when CRA reviews two full calendar years of remittances and notifies you in writing. A heavy single month doesn't change the class.

What's the penalty if I miss a remittance?

Penalties are graduated by lateness: 3% (1–3 days late), 5% (4–5 days), 7% (6–7 days), 10% (more than 7 days or never paid). Second or subsequent failures within the same calendar year can trigger a 20% penalty under the gross-negligence rule. Interest also accrues on the unpaid balance at the CRA's prescribed rate. The penalties apply to the gross remittance amount, not just the income-tax portion.

Do I need WorkSafeBC in addition to source deductions?

Yes, if you're a BC employer. WorkSafeBC is provincial workers' compensation and is separate from federal source deductions. Registration is required before the first day of work in most cases, and quarterly reporting is required even for nil periods. Other provinces have equivalents (WCB Alberta, WSIB Ontario, CNESST Quebec). The federal CRA source-deduction system doesn't replace this; you're responsible for both.

Can I just pay myself irregularly and true up at year-end?

The CRA says no. If you pay yourself salary in a given month, source deductions are owed on that salary by the next 15th. Trying to "true up" at year-end means the corporation has been holding employee money (yours) past the due date, which is exactly what the late-remittance penalty structure exists to discourage. The cleanest practice for incorporated owners drawing salary: pay yourself on a regular monthly schedule and remit on the same schedule. More on this in the Modern Books resource hub.

General information only — not tax or compliance advice. CRA rules, source-deduction rates, and remittance schedules apply to specific facts that aren't in this post. Modern Books and our sister firm Modern Axis CPA can review your situation; a blog post can't.