Financial Literacy

How to Read Your Balance Sheet: A Guide for Owners

May 25, 2026

You opened the PDF your bookkeeper sent. The P&L is on page 1. You scrolled past it to check the bottom line, closed the file, and called it month-end. The balance sheet is on page 3 — and it's the statement most owners ignore. It's also where solvency lives.

This post explains how to read your balance sheet as a Canadian small-business owner, what each section actually tells you, and the three numbers worth checking every month. No accounting degree required.

Key takeaways

The balance sheet shows what your business owns (assets), owes (liabilities), and what's left over for the owners (equity) at a single point in time. The P&L is a movie of the period; the balance sheet is a photograph at the end of it.

The accounting equation that ties it all together: Assets = Liabilities + Equity. If your balance sheet doesn't balance, the books are wrong somewhere — not the math.

The three numbers every owner should check monthly: working capital (current assets minus current liabilities), current ratio (current assets divided by current liabilities), and owner equity over time (whether the business is building or eroding value).

Accounts receivable, accounts payable, deferred revenue, and prepaid expenses all live on the balance sheet. If you're on accrual books, the balance sheet is where you see them; if you're on cash books, these accounts don't exist and the balance sheet tells you much less.

Owner equity moves for two reasons: profit (from the P&L flowing into retained earnings) and owner draws or dividends (cash going out to the owner). Track this line for the real picture of whether the business is gaining or losing value year over year.

What a balance sheet actually is

The balance sheet is a point-in-time snapshot of your business's financial position. If your year-end is December 31, your year-end balance sheet shows what the business owned, owed, and was worth at exactly 11:59 PM on December 31 — not what it did during the year. (Modern Axis's bookkeeping basics piece covers the broader financial-statements vocabulary if you want the foundational primer.)

The P&L is the opposite: it's the movie of the period. Revenue earned, expenses incurred, profit made between January 1 and December 31.

Both statements describe the same business but from different angles. The P&L tells you whether the business made money this year. The balance sheet tells you what the business looks like at the end of that year. The two are linked: net income from the P&L flows into retained earnings on the balance sheet, which is why a year of profit increases owner equity (assuming no big draws or dividends).

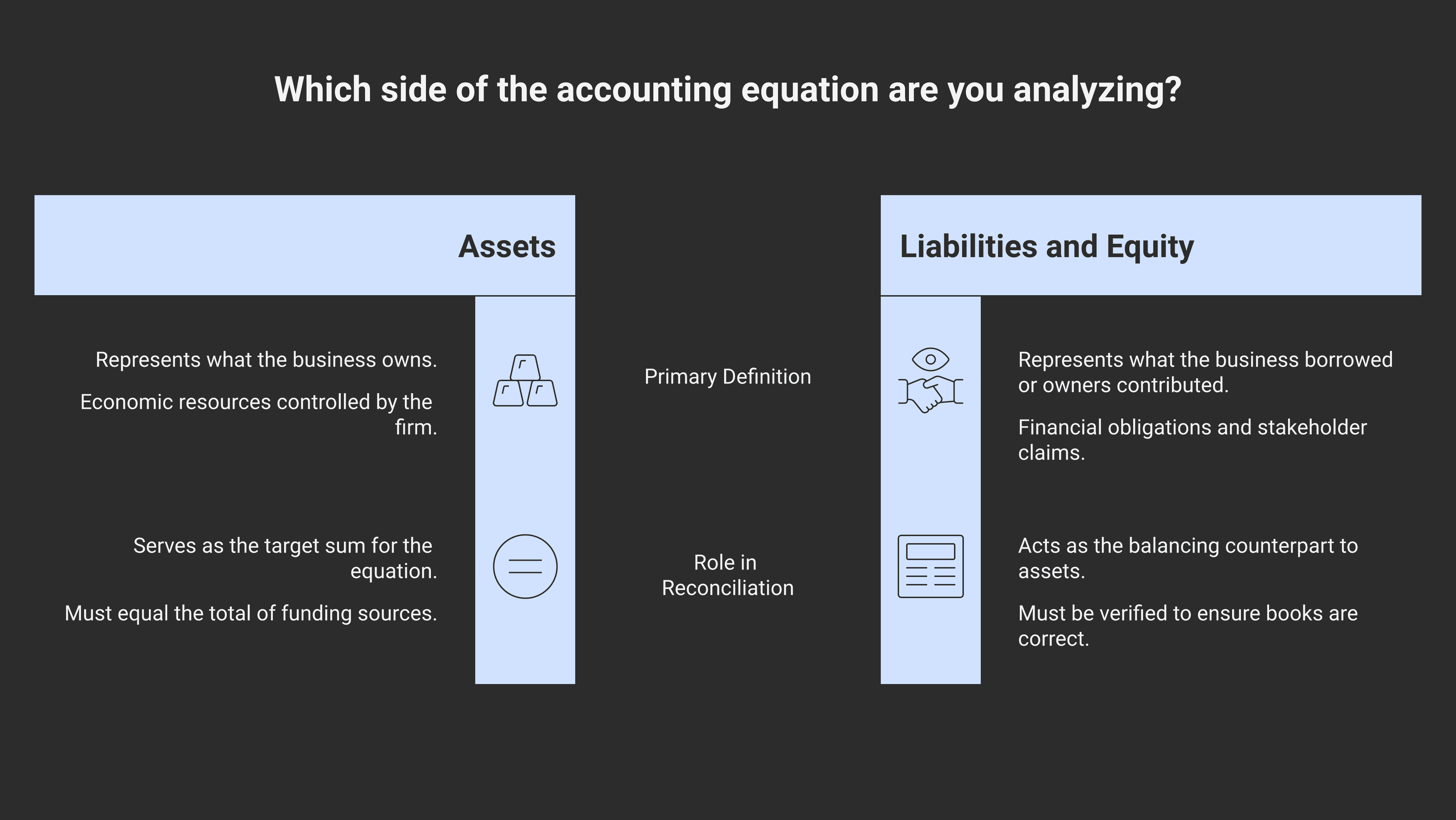

The accounting equation

Every balance sheet, anywhere in the world, follows one equation:

Assets = Liabilities + Equity

In plain English: everything the business owns was either borrowed (liabilities) or contributed by the owners (equity, including profit kept in the business). The two sides always balance. If they don't, the books are wrong — a missed entry, a duplicate posting, or a misclassified transaction.

The "balance" in "balance sheet" is literal. A bookkeeper's first reconciliation check every month is whether the balance sheet balances. It always should. When it doesn't, that's the first thing to fix.

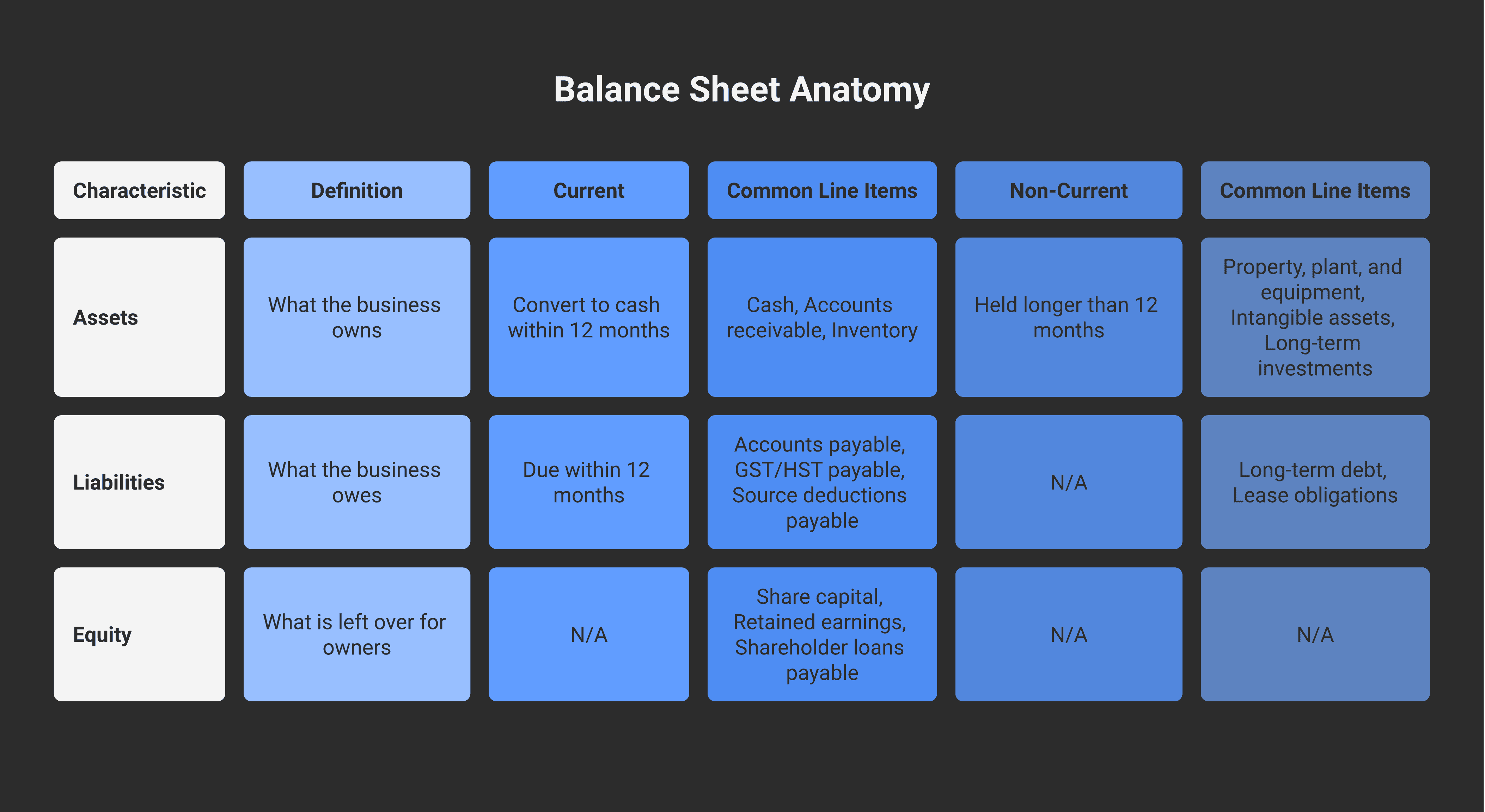

The three sections, line by line

Assets — what the business owns

Split into current and non-current (also called "long-term" or "fixed").

Current assets (expected to convert to cash within 12 months):

Cash and cash equivalents — chequing accounts, savings, GICs that mature within a year

Accounts receivable — invoices issued but not yet paid (only exists on accrual books)

Inventory — finished goods, work in progress, raw materials, valued at the lower of cost or net realizable value

Prepaid expenses — payments made for something you'll consume over time (annual insurance, prepaid software, prepaid rent)

GST/HST receivable — input tax credits owed back to you by the CRA (when ITCs exceed collected GST)

Non-current assets (held for more than 12 months):

Property, plant and equipment — vehicles, machinery, computers, leasehold improvements, at original cost minus accumulated depreciation

Intangible assets — goodwill, trademarks, software licences, patents

Long-term investments — securities held longer than a year, minority interests in other corporations

Liabilities — what the business owes

Same split: current and non-current.

Current liabilities (due within 12 months):

Accounts payable — bills received but not yet paid (only exists on accrual books)

GST/HST payable — net sales tax owed to CRA after subtracting input tax credits

Source deductions payable — CPP, EI, and income tax withheld from employees and not yet remitted (see our source-deductions post)

Deferred revenue — cash collected for something you haven't yet earned

Current portion of long-term debt — the principal portion of a multi-year loan due within the next 12 months

Credit card balances

Non-current liabilities (due beyond 12 months):

Long-term debt — equipment loans, mortgages, shareholder loans, beyond the current portion

Lease obligations — capitalized lease liabilities

Equity — what's left over

For a sole proprietor, equity is one line: Owner's equity or Owner's capital, which moves with profit and owner draws.

For a corporation, equity splits into three:

Share capital — what shareholders paid in for their shares

Retained earnings — accumulated net income minus dividends paid out over the life of the corporation

Shareholder loans payable — money the owner has loaned in to the corporation (sometimes shown in liabilities; some accountants put it in equity)

For corporations using a holdco structure, the Modern Axis holding companies post is the deeper version of how equity moves between operating company and holdco.

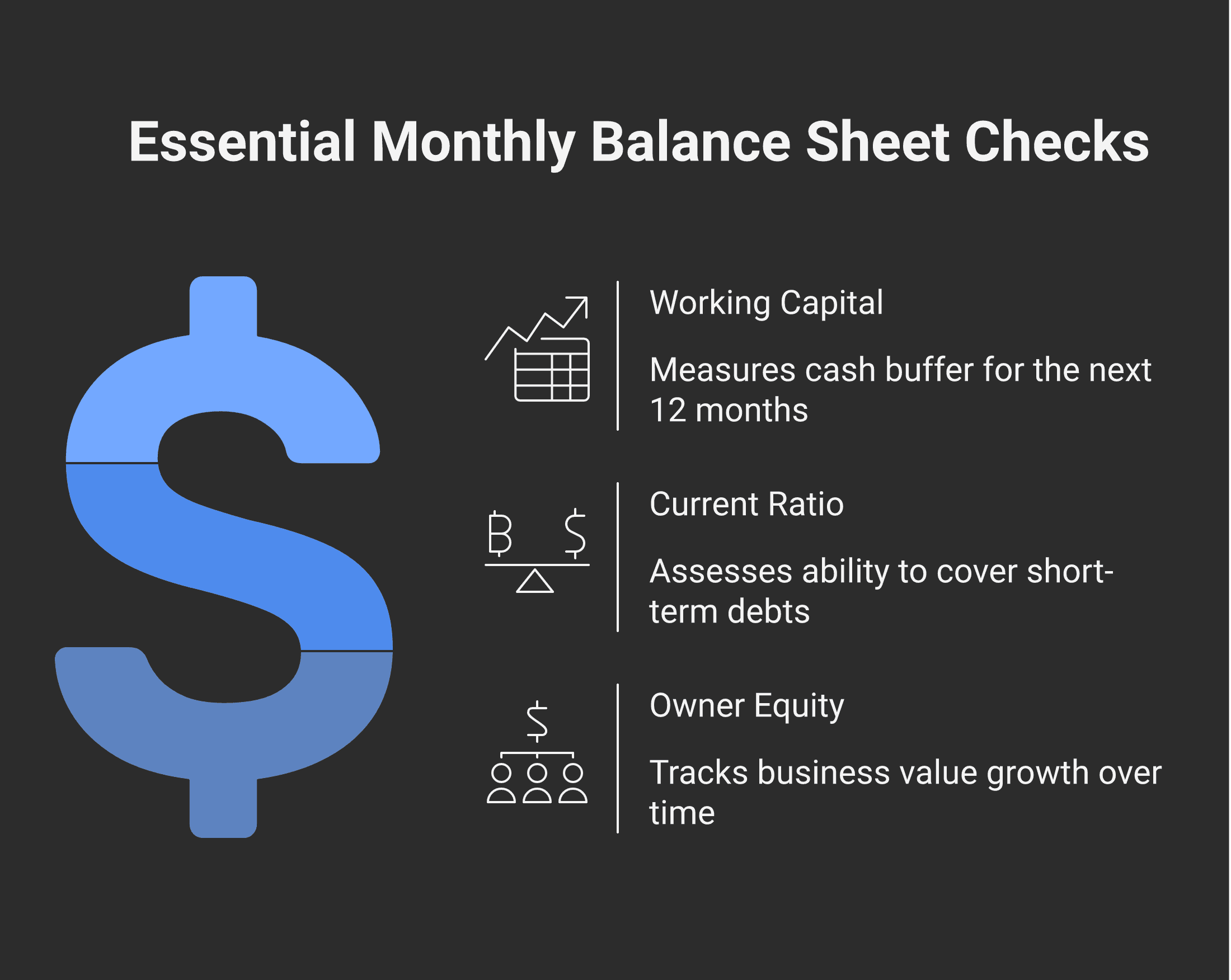

The three numbers every owner should check

Most owners can ignore most balance sheet lines most of the time. These three move the needle:

Working capital

Current assets minus current liabilities.

This is the cash buffer your business has to survive the next 12 months. Positive working capital means you can pay your near-term obligations from your near-term resources. Negative working capital is a warning — you're relying on future sales or new financing to cover what you already owe.

A typical small business wants positive working capital. The exact amount depends on your industry and your seasonality — a retailer with heavy inventory pre-Christmas needs more than a service business with no inventory at all.

Check working capital monthly. A consistent downward trend over 3–4 months is something to ask the bookkeeper about.

Current ratio

Current assets divided by current liabilities.

The same idea expressed as a ratio. A current ratio of 1.0 means you have exactly enough current assets to cover current liabilities. Most growing businesses target 1.5 to 2.0.

A current ratio under 1.0 is a yellow light. Under 0.8 is a red light. A current ratio over 3.0 might mean you're sitting on too much cash that could be deployed back into the business.

Owner equity over time

Look at the equity section at this month-end compared to the same line 12 months ago.

If equity has grown, the business made money and you didn't take all of it out. If it's flat, you took out roughly what you earned. If it's down, you took out more than you earned — which sometimes happens (year-end bonuses, life events) but should not be a recurring pattern.

Equity over time is the closest single number to "is the business actually worth more than it was a year ago" — assuming you're on accrual books and your accountant has done the year-end close properly. On cash books, equity changes are partially fictional, which is one more reason to be on accrual.

Where the balance sheet ties to your bank account

The balance sheet shows "cash and cash equivalents" at the top of the asset section. That number should match your bank reconciliation as of the same date. Within rounding (a few cents) and outstanding cheques or deposits, the cash on your balance sheet equals what's in the bank.

If they don't match, your bookkeeper hasn't reconciled. That's the single most common bookkeeping failure on DIY books — the bank shows $42,000, the balance sheet shows $48,000, and nobody's checked. The $6,000 gap is usually some combination of unreconciled deposits, missed bank fees, and uncategorized transactions.

A clean balance sheet ties to the bank to the penny (or close to it) every month. If you can't see that match in your books, ask the bookkeeper.

Incorporated vs unincorporated balance sheets

A sole proprietor balance sheet has a single owner's equity line. The business and the owner are legally the same person; the balance sheet just tracks what's "in" the business at any moment.

A corporation balance sheet has share capital + retained earnings + (sometimes) shareholder loans separated out. The business is a legal entity distinct from the owner, which means:

Money the owner puts in is either share capital (formal — increases ownership stake) or a shareholder loan (informal — increases liability to the owner)

Money the owner takes out is either a dividend (reduces retained earnings) or a shareholder loan repayment (reduces the loan liability) or a salary (an expense on the P&L)

The Modern Axis small business deduction post covers how the corporate balance sheet ties into the SBD rules — passive investment income on the balance sheet can affect SBD eligibility past a certain threshold

The corporate balance sheet has more moving parts. It also tells you more about what the business is worth as a separate entity.

What to ask your bookkeeper when something looks off

If you're looking at your balance sheet monthly and a number looks wrong, a few questions to ask:

Why does cash on the balance sheet not match my bank account? Most common cause: unreconciled bank feed. Should be fixed in the next month-end close.

What's in "Suspense" or "Uncategorized"? Many bookkeeping software packages have a holding account for transactions that couldn't be matched automatically. Anything sitting there for more than 30 days is a problem.

Is accounts receivable growing faster than revenue? A sign that collections are slowing — invoices going out but not being paid on time.

Is accounts payable growing? A sign that you're stretching suppliers, intentionally or otherwise.

Did retained earnings drop without a dividend or distribution? A prior period adjustment was made — ask what changed.

If the bookkeeper can't answer one of these in a sentence, the books are likely behind on reconciliation.

When clean books make the balance sheet usable

Modern Books reconciles every account on the balance sheet monthly — cash to the bank, AR to the invoice subledger, AP to the bill subledger, deferred revenue to active customer contracts, GST/HST to the filing position. The deliverable is a balance sheet that ties to underlying records and tells you something true about the business. Modern Books' Mid and Growth tiers include monthly financials with that level of reconciliation. More balance-sheet reading and bookkeeping fundamentals in the resource hub.

Frequently asked questions

What is a balance sheet in simple terms?

A balance sheet is a point-in-time snapshot of what your business owns (assets), owes (liabilities), and what's left over for owners (equity). It follows the equation Assets = Liabilities + Equity, which always balances. While the P&L tells you whether the business made money during a period, the balance sheet tells you what the business looks like at the end of that period.

How often should I look at my balance sheet?

Monthly, at minimum, the same day you review the P&L. Quarterly for businesses with simple operations and minimal balance-sheet activity. Annual review is too infrequent for any business with inventory, receivables, payables, or shareholder loans — issues that compound monthly become expensive cleanup at year-end.

What's working capital and why does it matter?

Working capital is current assets minus current liabilities — the cash buffer your business has to cover near-term obligations. Positive working capital means you can pay what you owe in the next 12 months from what you'll collect or convert in the next 12 months. Negative working capital is a warning sign that you're relying on future activity or new financing to cover existing obligations.

What's a good current ratio for a small business?

Most growing small businesses target a current ratio of 1.5 to 2.0 (current assets 1.5× to 2× current liabilities). Under 1.0 is a yellow flag — you can't cover your current liabilities from current assets. Over 3.0 might mean you're sitting on idle cash that could be redeployed. Industry context matters: retailers with heavy inventory need more buffer than service businesses with no inventory.

Why doesn't the cash on my balance sheet match my bank account?

Almost always: the bookkeeper hasn't completed the monthly bank reconciliation. The balance sheet shows the book balance (transactions recorded in the books), the bank shows the bank balance (transactions cleared by the bank), and the difference is timing — outstanding cheques, deposits in transit, unreconciled bank fees. A clean monthly reconciliation should resolve this to within a few cents.

What's the difference between equity and profit?

Profit is from the P&L — what the business earned in the period. Equity is on the balance sheet — what the business is worth to the owner at a point in time. They're linked: net income flows from the P&L into retained earnings (an equity account). Equity also moves down when owners take money out (draws or dividends). Equity up = profit minus distributions. Track it over 12-month windows.

How does my balance sheet relate to my tax return?

Your year-end balance sheet is part of your corporate tax return (T2) — Schedule 100 reports the balance sheet, Schedule 125 reports the P&L. For sole proprietors, the balance sheet isn't required on the T1 directly, but the year-end equity figures inform the next year's opening balances. Most accountants will request a balance sheet alongside the year-end financials regardless of business structure.

Should I be on accrual books to get a useful balance sheet?

Yes. Cash books don't track accounts receivable, accounts payable, deferred revenue, or prepaid expenses — which are most of what makes a balance sheet useful. A cash-method balance sheet shows cash, equipment, and equity, and not much else. The moment you have outstanding invoices or unpaid bills, you need accrual books to see the real picture. See our cash vs accrual post for when the switch makes sense.

This post covers general bookkeeping practice in Canada and isn't bookkeeping advice for your business. The right setup for your specific business depends on facts not covered above. Talk to a bookkeeper or CPA who knows your numbers before relying on anything you've read here.