Business Operations

When You Need an Accountant, Not Just a Bookkeeper

May 25, 2026

You've outgrown DIY books. You hired a bookkeeper. The books are clean for the first time in two years. Then April comes, your tax preparer asks four questions you don't know the answers to, your bookkeeper says "that's an accountant question," and you realize the two are not the same role. This is the moment most growing Canadian businesses figure out they need both.

This post covers what bookkeepers actually do, what accountants actually do, where the line is, when you cross it, and why most growing businesses need both rather than choosing.

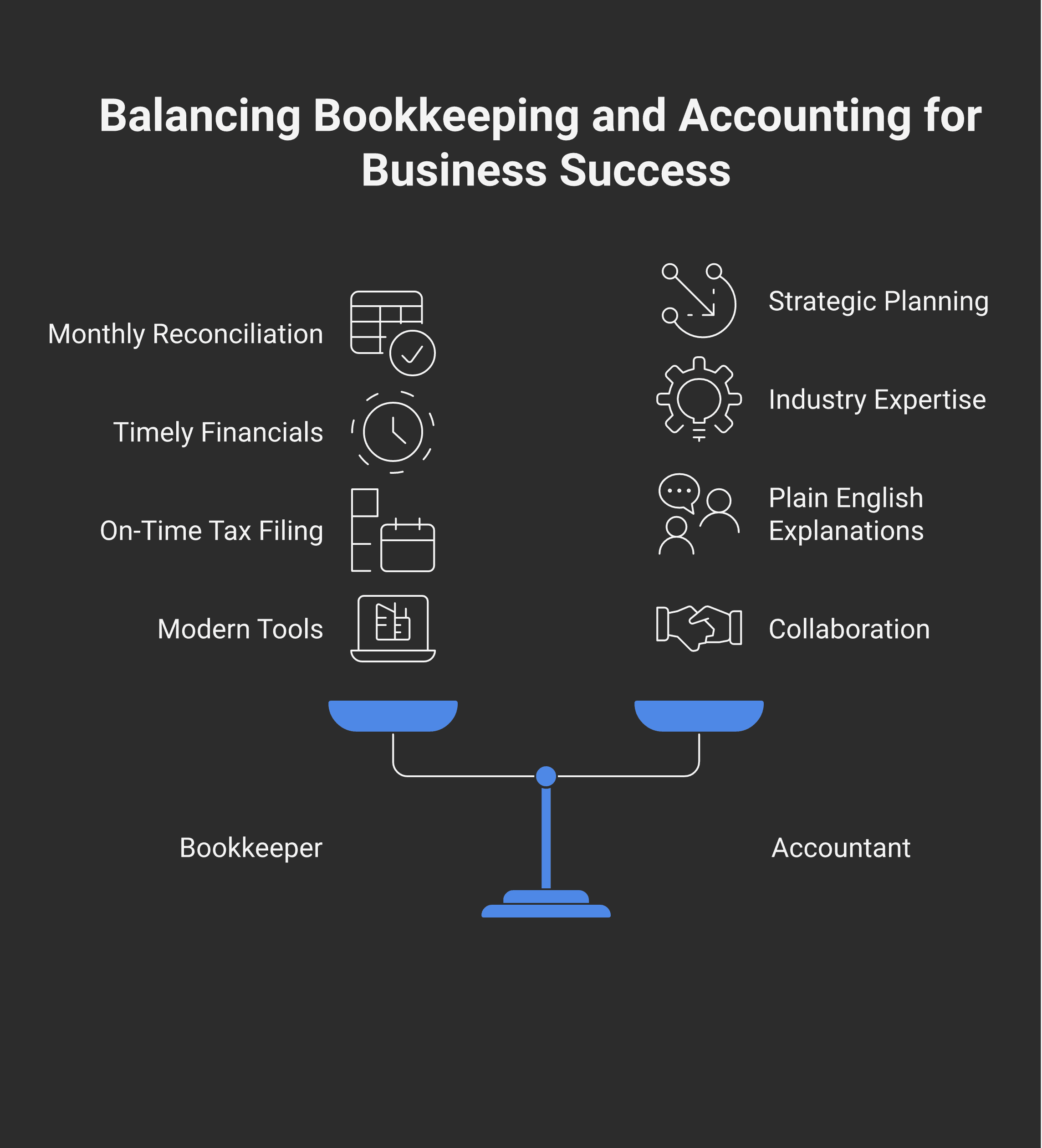

Key takeaways

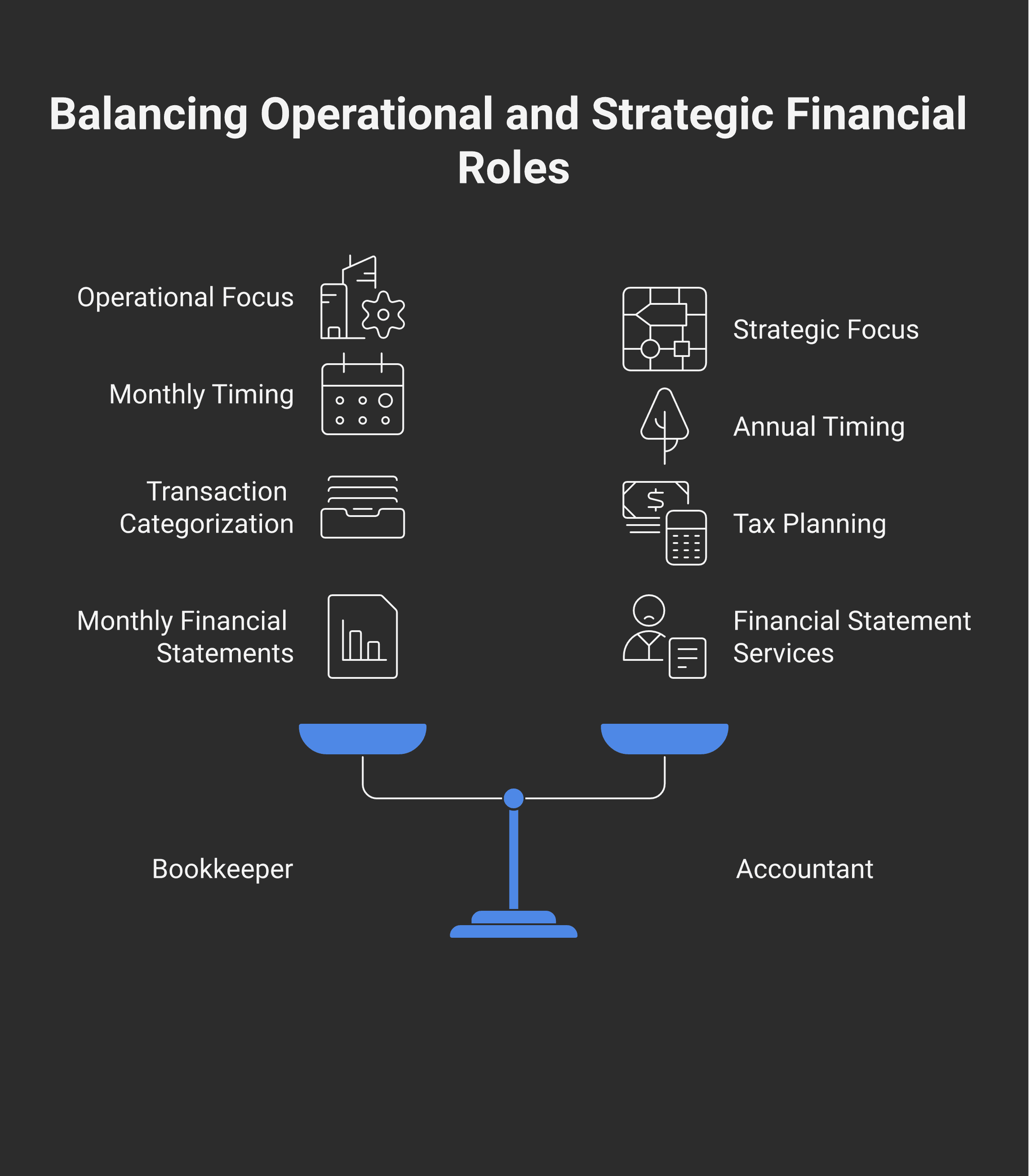

Bookkeepers handle the operational record — categorizing every transaction, reconciling accounts, running payroll, processing GST/HST filings, producing monthly financials. The deliverable: clean books and accurate monthly reports.

Accountants handle the strategic and compliance layer — tax planning, year-end close, corporate tax (T2) filing, financial-statement preparation for the bank, structural advice (incorporation, holdco, family trust). The deliverable: tax-optimized outcomes and decisions that affect more than the current period.

You need a bookkeeper from day one of any business with more than a handful of transactions a month. You need an accountant the moment a decision crosses into tax strategy, structure, or multi-year planning — typically by year 2 or sooner if you incorporate.

The two roles are complementary, not competing. A clean bookkeeper hands the accountant clean books; the accountant builds on them. The friction in growing businesses is usually one role missing, not too many.

Designation matters at the accountant level. A Chartered Professional Accountant (CPA) has regulatory accountability, professional liability insurance, and the right to sign off on financial statements for third parties (banks, CRA, investors). Bookkeepers don't need to be CPAs; accountants reviewing your year-end usually should be.

What a bookkeeper actually does

A bookkeeper's job is the operational record of the business. The transactions, the reconciliations, the filings that recur every month. Concretely:

Categorize every transaction from bank feeds, credit cards, and uploaded receipts into the chart of accounts

Reconcile each account monthly — bank, credit card, loans, payment processors (Stripe, Square, Shopify payouts), against statements

Run payroll — calculate gross to net, remit source deductions by the 15th of the next month, issue T4s at year-end

File GST/HST returns based on the period's collected vs paid

Manage accounts receivable and payable — record invoices, track aging, process bill payments

Produce monthly financial statements — P&L, balance sheet, cash flow — clean and ready for the owner to review

Maintain the chart of accounts so the reports tell the owner something useful

Provide year-end-ready books to the accountant — a trial balance, reconciled accounts, and supporting documentation

The bookkeeper's lens: what happened. The owner gets accurate monthly numbers; the accountant gets a clean handoff. The bookkeeper doesn't advise on the salary-vs-dividend mix, doesn't decide whether to incorporate, and doesn't sign off on financial statements for the bank.

A good bookkeeping engagement runs without you thinking about it. The bank feeds flow, the reconciliations happen, the financials land in your inbox monthly. That's the win.

What an accountant actually does

An accountant's job is the strategic and compliance layer that sits on top of the operational record. Concretely:

Tax planning — when to take salary vs dividend, when to incorporate, when to set up a holdco, when to elect into or out of various provisions, RRSP and TFSA strategy alongside the business

Year-end close and adjustments — accruals, deferrals, depreciation (CCA), shareholder loan reconciliation, opening-balance verification, closing entries

Corporate tax filing (T2) — preparing and filing the corporation's return, including all schedules, and dealing with CRA correspondence on review

Personal tax filing (T1) for the owner — especially for owner-managers where the corporate and personal returns interact

Financial-statement preparation at the compilation, review, or audit level — for banks, investors, or formal reporting

Structural advice — whether to incorporate, whether to set up a holding company, how to integrate a family trust, when to pay off a shareholder loan vs declare a dividend

Multi-year planning — capital gains exemption planning, business sale preparation, retirement and succession

CRA representation — handling reviews, audits, voluntary disclosures, and disputes

The accountant's lens: what should happen. Strategy, structure, compliance, multi-year horizon. The accountant builds on the bookkeeper's clean record to make decisions the bookkeeper doesn't have the licensure or scope to make.

Where the line actually is

Five concrete cases where the line crosses from bookkeeping to accountant territory:

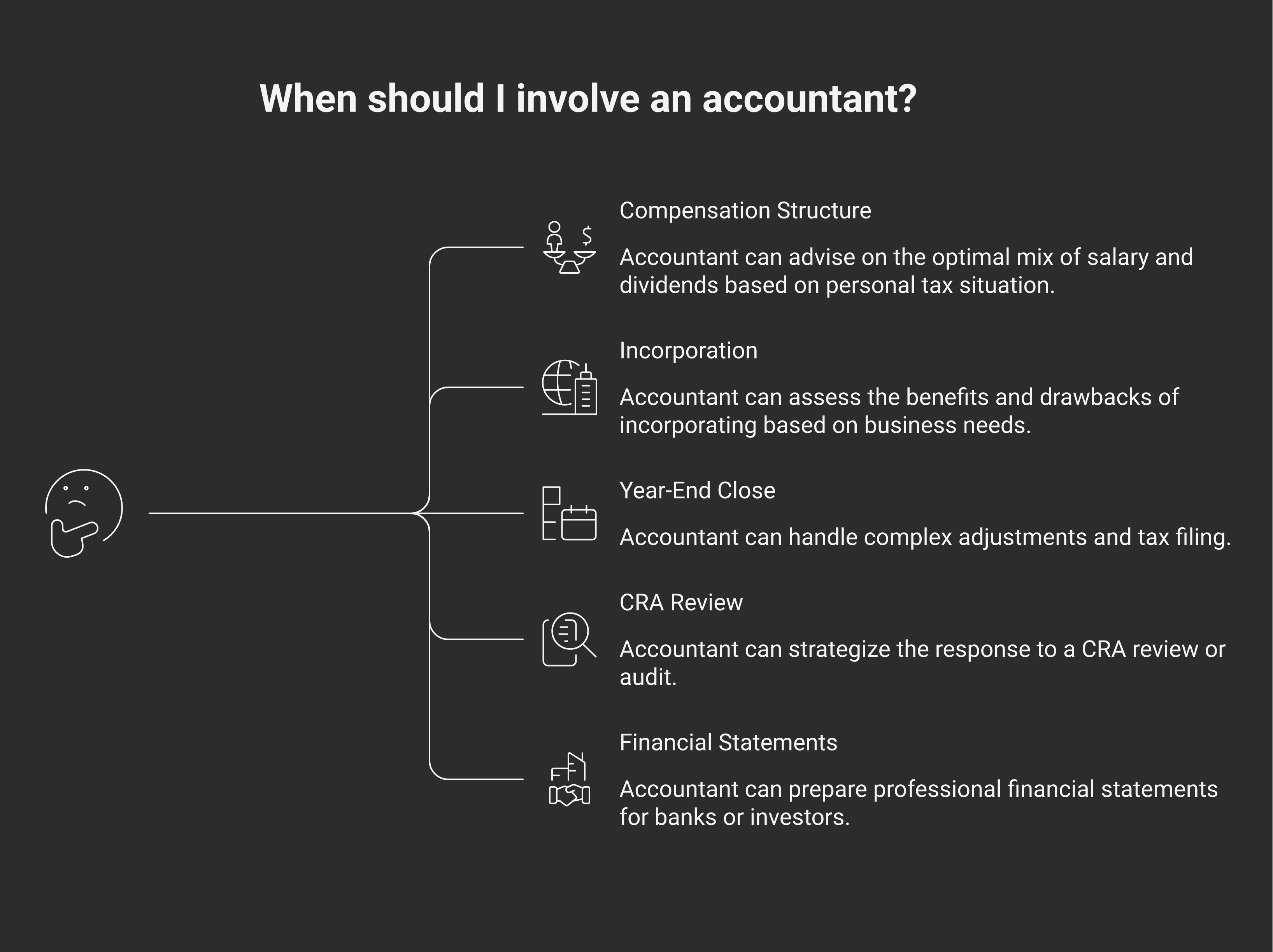

1. Choosing your compensation structure

Your bookkeeper runs payroll for whatever salary number you set. Your bookkeeper records dividends when you declare them. The bookkeeper doesn't pick the salary-vs-dividend mix — that decision depends on your personal tax bracket, RRSP room, CPP planning, family income split, and a half-dozen other variables. Accountant question.

2. Deciding whether to incorporate

Your books can run in either structure. The bookkeeper executes either. The decision turns on: net income level, liability exposure, integration math, the small business deduction, future sale plans, family income splitting. None of that is operational. Accountant question.

3. Year-end close and tax filing

Your bookkeeper produces a year-end trial balance. The accountant takes it from there: depreciation entries (CCA classes), accruals for unpaid bonuses or year-end expenses, shareholder loan adjustments, the T2 (or T1 with T2125), all the schedules. This is the hand-off point. Accountant work.

4. A CRA review or audit

A CRA review letter lands. Your bookkeeper can produce the supporting documentation the books generated — receipts, invoices, payroll registers, bank reconciliations. The strategic response — what to submit, what to argue, when to negotiate, when to invoke the Voluntary Disclosures Program — is accountant territory.

5. A bank or investor needs financial statements

When a bank wants statements for a loan or refinance, or an investor wants statements for due diligence, the bookkeeper's monthly P&L isn't enough. The bank wants a compilation, review, or audit signed by a licensed professional — typically a CPA. The bookkeeper produces the data; the accountant produces the signed statements.

Why most growing businesses need both

The friction most growing Canadian businesses experience isn't "too many accountants." It's a missing role.

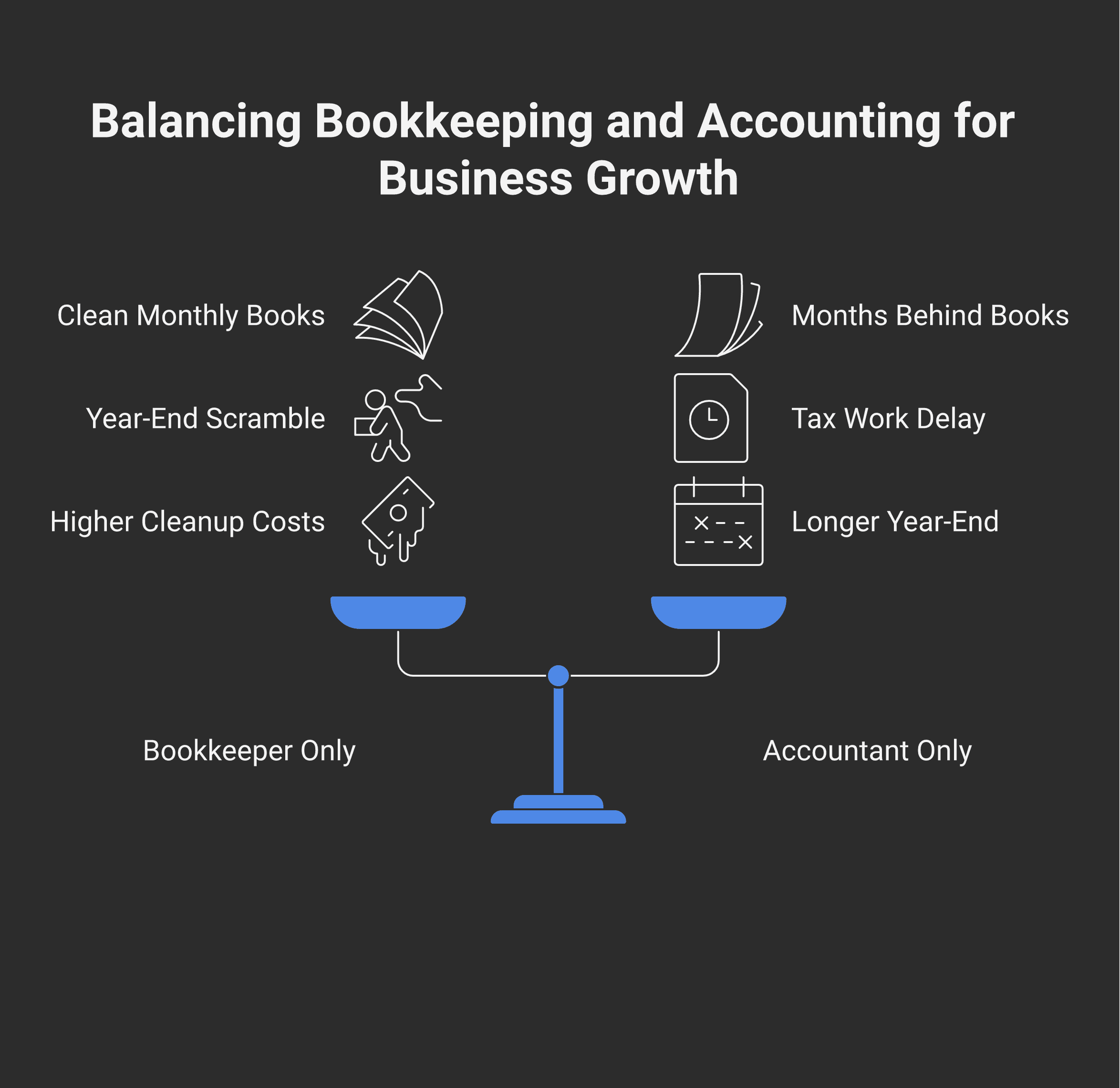

Pattern 1 — Bookkeeper only, no accountant. The books are clean monthly. Year-end arrives and the owner scrambles to find an accountant to do the T2. The accountant inherits books that are operationally clean but not tax-optimized — the salary-vs-dividend mix was random, the shareholder loan account is messy, no CCA was tracked through the year. The cleanup costs more than a year of monthly accountant consultation would have.

Pattern 2 — Accountant only, no bookkeeper. The owner DIYs the books or the books are months behind. The accountant has to do bookkeeping cleanup before they can do tax work. The bill is large, the year-end takes months, and the owner has no usable monthly financials in the meantime.

Pattern 3 — Both, working together. The bookkeeper produces clean monthly books. The accountant sets strategy at year-end and reviews quarterly. The owner gets the operational deliverable monthly and the strategic deliverable at the year-end and milestone moments. The total cost is lower than either pattern 1 or pattern 2 — because the work doesn't have to be redone.

The economics are clear: a bookkeeper at $200–$400/month plus an accountant at year-end is cheaper, faster, and produces better outcomes than either role alone trying to cover both lanes.

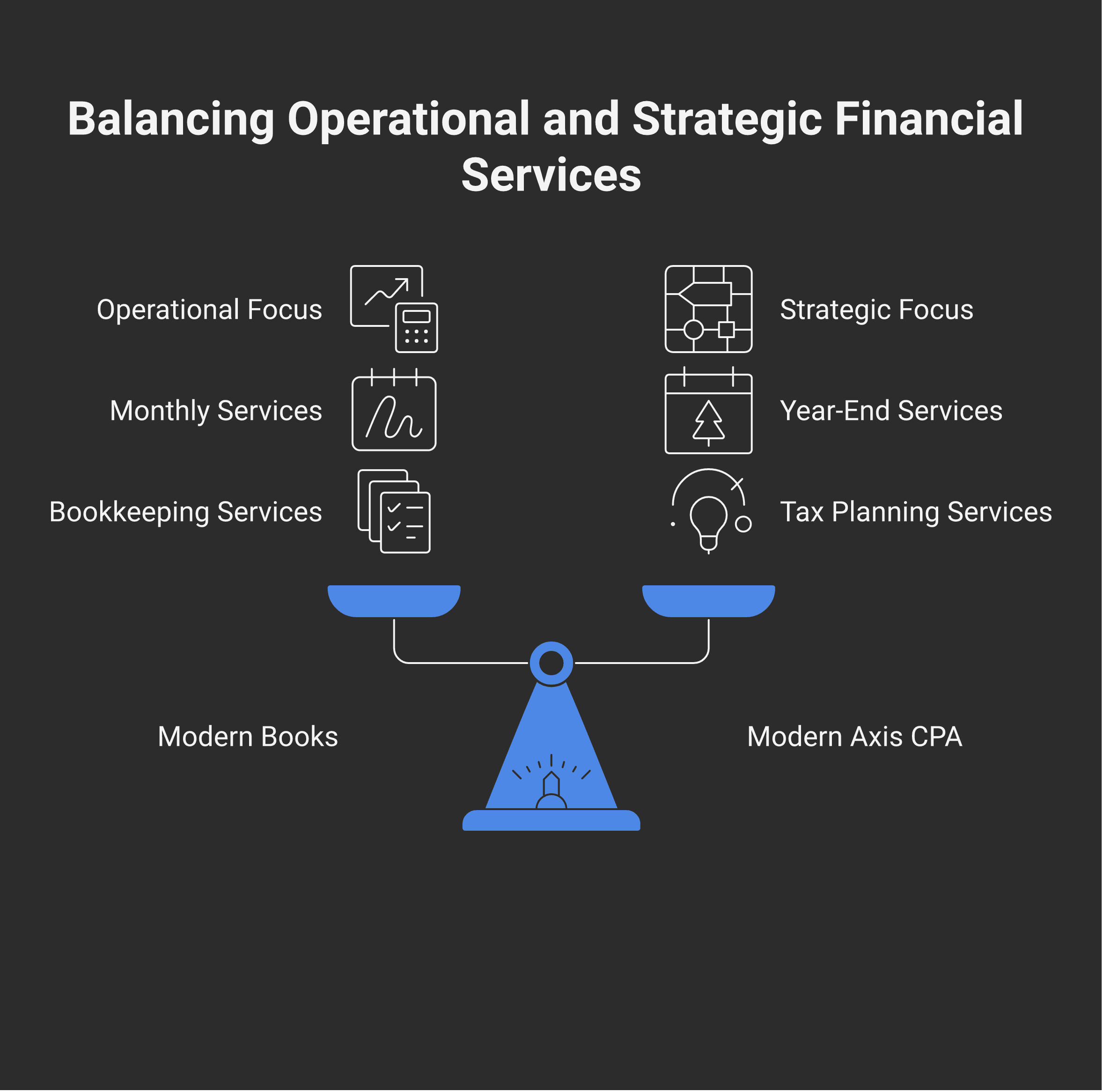

How Modern Books and Modern Axis work together

Modern Books handles the operational layer — monthly bookkeeping, payroll, GST/HST filings, monthly financials. Modern Axis CPA, the sister firm, handles the strategic and compliance layer — tax planning, corporate tax filing, structural advice, fractional controller services for businesses past bookkeeping-only size, cross-border tax for US persons in Canada and Canadians with US exposure.

The two share the same firm, the same systems, and the same client record. A Modern Books client can escalate to Modern Axis when the bookkeeping conversation turns into a tax-strategy conversation, without changing software, changing firms, or re-onboarding. The handoff is internal.

When a Modern Books client outgrows bookkeeping-only — typically when they incorporate, when revenue crosses the small-business-deduction relevance threshold, when they're considering a holdco or a family trust, or when they get a CRA review — the Modern Axis CPA team picks up the strategic side directly. Same firm, broader scope.

What to look for in each

A good bookkeeper:

Reconciles every account monthly, every account, to the penny

Hands you monthly financials on a predictable cadence (within 10–15 days of month-end is the standard target)

Maintains a clean chart of accounts and a documented categorization policy

Files GST/HST and source-deduction returns on time, every time

Uses modern tools — Dext, HubDoc, QuickBooks Online, Xero — not a shoebox

Knows when something is an accountant question and tells you

A good accountant:

Is a licensed CPA (the bookkeeper doesn't need to be; the accountant should be)

Talks to you about strategy at least once a year, not just at filing time

Can speak to your industry, your structure, and your specific circumstances

Coordinates with your bookkeeper rather than redoing their work

Files on time and explains decisions in plain English

Tells you when you've outgrown them, too

The bookkeeper and accountant should know each other and talk to each other. The best engagements feel like one team with two specialties, not two vendors competing for the same workload.

When you'd ask Modern Books to start the engagement

If you're at the "I need clean monthly books" stage, that's where Modern Books begins. The Mid and Growth tiers cover monthly bookkeeping plus payroll plus quarterly reporting; the Starter tier is for sub-25-transaction businesses with annual reporting needs. When the engagement crosses the line into tax strategy, the Modern Axis side picks it up directly. Book a session if you want to talk through what fits your current stage. More posts on bookkeeping practice in the Modern Books resource hub.

Frequently asked questions

What's the difference between a bookkeeper and an accountant in Canada?

A bookkeeper handles the operational record — categorizing transactions, reconciling accounts, running payroll, filing GST/HST, producing monthly financials. An accountant handles the strategic and compliance layer — tax planning, year-end close, corporate (T2) filing, financial-statement preparation, structural advice. The two are complementary; growing businesses typically need both.

Can a bookkeeper do my taxes?

Bookkeepers can prepare T1 returns for individuals and T2125 schedules for sole proprietors. They generally don't prepare corporate (T2) returns for incorporated businesses, and they don't sign off on financial statements that go to banks or investors. Anything that requires professional sign-off — financial statements, complex tax positions, CRA representation — needs a CPA.

When do I need to hire an accountant?

By the time you incorporate, almost certainly. Often sooner. A sole proprietor with simple operations can use a bookkeeper for T1 prep through year 1 or 2, but the moment you cross into corporate structure, multi-year planning, family income splitting, holding companies, or cross-border situations, accountant work begins. The cleanest rule: hire an accountant before incorporation, not after.

Is a CPA the same as a bookkeeper?

No. CPA (Chartered Professional Accountant) is a regulated designation requiring specific education, exams, articling, and ongoing professional development. CPAs are licensed by provincial bodies (CPABC in BC, CPA Ontario, etc.), carry professional liability insurance, and can sign off on financial statements. Bookkeepers don't need a designation in Canada — though many have certifications like CPB (Certified Professional Bookkeeper).

Can I outsource bookkeeping but do my own taxes?

You can. It works for very simple sole-prop situations. The moment you incorporate, the math changes — the T2 return, schedules, CCA tracking, salary-vs-dividend planning, and shareholder loan management quickly outpace what's reasonable to DIY. Most incorporated owners who try end up paying an accountant for cleanup that exceeds what proper engagement would have cost.

How much should I budget for both?

A bookkeeper for a small business typically runs $200–$600/month depending on transaction volume. An accountant for an incorporated small business typically runs $2,000–$5,000/year for the T2 and annual planning, plus $200–$500/hour for additional consultation. The combined annual cost for a growing incorporated business is usually $5,000–$12,000 — and produces better outcomes than either role alone trying to cover both.

Why can't one person do both for a small business?

Some people can — typically CPAs running solo practices who do both bookkeeping and tax work. It works for very small clients. As the business grows, the lanes diverge: bookkeeping is high-frequency, low-strategy operational work; tax is low-frequency, high-strategy work. Specialization wins as scale grows. The model where Modern Books handles the operational layer and Modern Axis CPA handles the strategic layer is built around this divergence.

What's the handoff between bookkeeper and accountant supposed to look like?

The bookkeeper delivers a year-end package: reconciled trial balance, supporting schedules (AR aging, AP aging, fixed asset register, shareholder loan continuity, GST/HST reconciliation), the year's bank and credit card reconciliations, and source-deduction year-end summary. The accountant takes that and does the year-end adjustments, schedules, and T2 filing. Both should be looking at the same chart of accounts in the same system.

General information only — not tax or accounting advice. The right combination of bookkeeping and accounting services depends on your business size, structure, and specific circumstances. Talk to a CPA who can review your situation before deciding what level of engagement you need.